Inside Chime's Growth Engine

Executive Summary

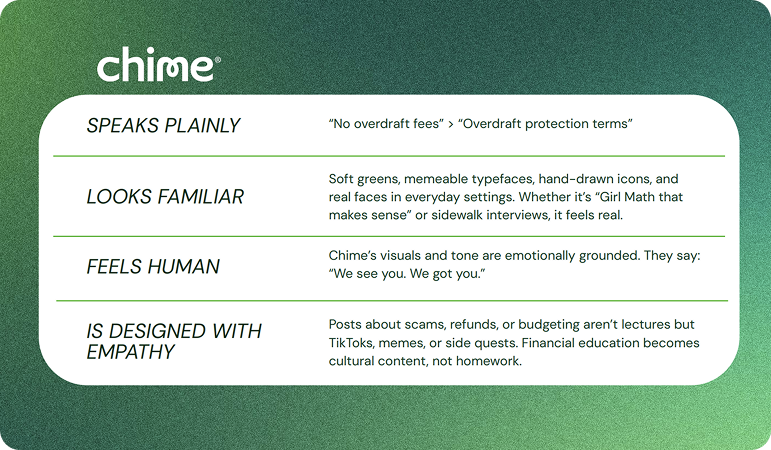

Chime didn't win by building a better bank. It won by building a more relatable one. Its meteoric rise in the US banking landscape wasn’t just about a better digital experience but a strategic mix of audience-first products, creator-powered storytelling, and platform-native brand behaviour. Chime’s growth is built on meeting the needs of a much broader reality, reaching millions of consumers who feel financially precarious or excluded by traditional systems.

We analysed our datasets to uncover trends which we translated into actionable recommendations for financial services marketers and leaders.

In a rush? Skip to the end for our 90-180 day action plan.

Key takeaways

- Chime’s real audience isn’t who you think. While positioned as a solution for tech-savvy urbanites, Chime over-indexes in overlooked cities and underserved communities. It built a banking experience not just for consumers but with them.

- Social fluency is Chime’s moat. Chime thrives where culture happens: TikTok, Reddit, Snapchat, by not just showing up but by sounding native. It speaks the language of its consumers, not the language of lenders, building emotional relevance faster than traditional financial institutions’ polished campaigns.

- Chime operationalized empathy. Every feature - early pay, no fees, real-time notifications - solves a real pain point. The magic isn’t complexity. It’s clarity, dignity, and frictionless design.

- Canada is next. Chime may have started in the US, but the conditions driving its rise – financial anxiety & a distrust in traditional finance – are playing out globally

The questions we answered

In 2025, the financial landscape is undergoing a rapid transformation, driven by disruptors like Chime. This report delves into Chime's growth engine and its challenge to traditional banking models, examining how it has shifted industry dynamics, reshaped audience expectations, and created a unique playbook.

To provide actionable insights for financial institutions navigating this change, we answer the following questions:

- How is Chime’s rapid growth redefining the financial landscape, and what can financial institutions learn from its playbook to stay competitive?

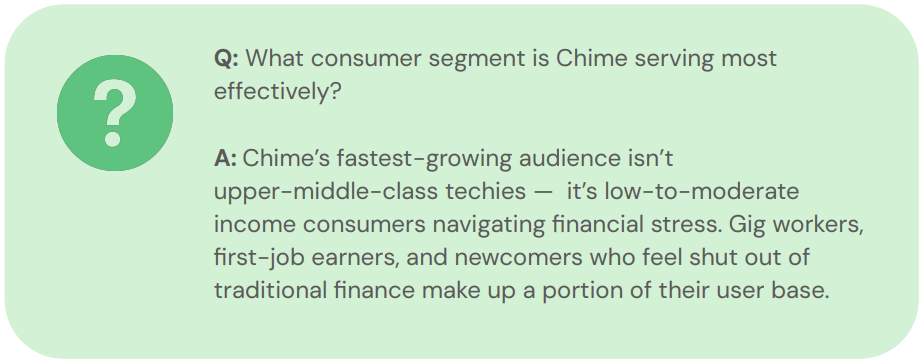

- What consumer segment is Chime serving most effectively, and why does this audience matter?

- How has Chime tailored its products, positioning, and content to resonate with the underbanked?

- What content strategies and creative themes drive adoption and trust with Chime’s audience?

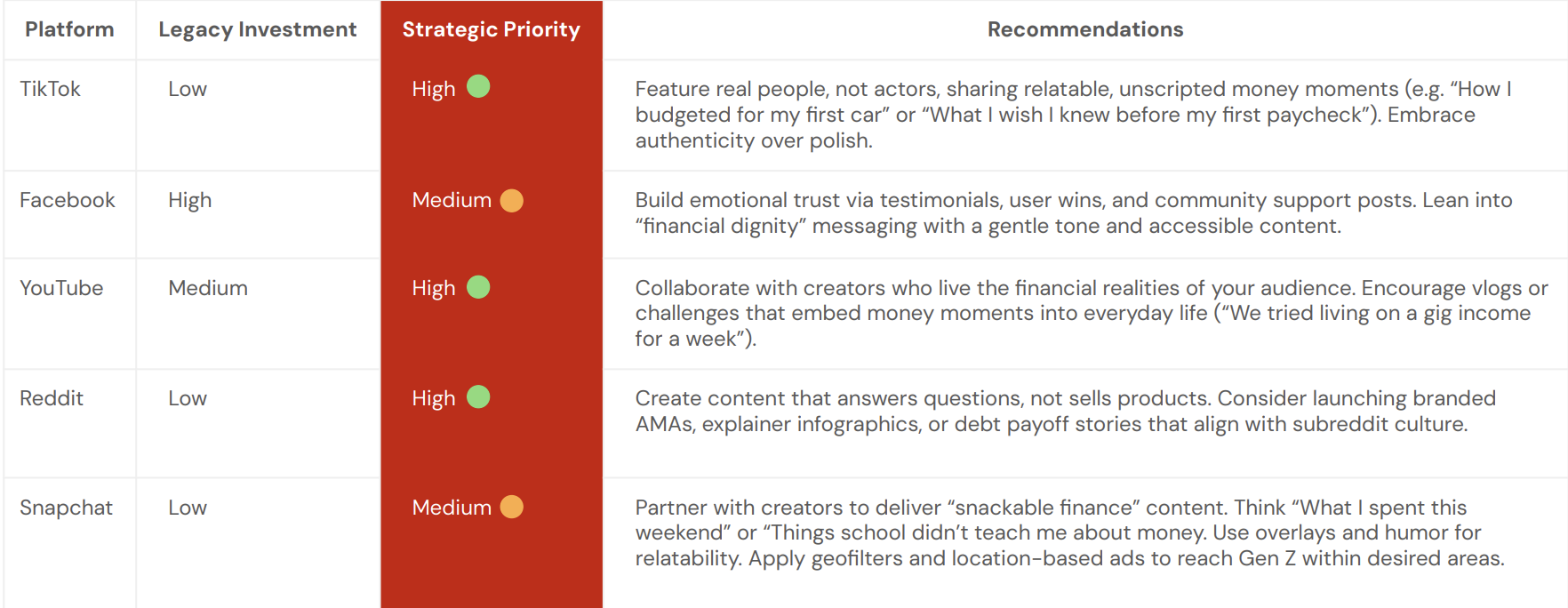

- Which social and digital platforms are most effective for Chime, and how do these choices differ from traditional financial brands?

- What brand partnerships, creators, and media strategies have powered Chime’s growth?

- Where are traditional financial institutions falling short? What tactical shifts could help them reclaim share?

- What are the whitespace opportunities for Canadian financial institutions to adapt this playbook to their markets?

How this report was created

This report was created by RightMetric’s expert research team, who looked deep into our datasets by leveraging over 25+ powerful data gathering tools. By weaving together various digital data points,, including audience demographics, behaviour, engagement metrics, and advertising campaigns, we are able to spot trends and opportunities.

We then employed proprietary methodologies to refine raw data and craft reports that tell the full story, delivering clear and actionable insights.

- How is Chime’s rapid growth redefining the financial landscape, and what can financial institutions learn from its playbook to stay competitive?

- What consumer segment is Chime serving most effectively, and why does this audience matter?

- How has Chime tailored its products, positioning, and content to resonate with the underbanked?

- What content strategies and creative themes drive adoption and trust with Chime’s audience?

- Which social and digital platforms are most effective for Chime, and how do these choices differ from traditional financial brands?

- What brand partnerships, creators, and media strategies have powered Chime’s growth?

- Where are traditional financial institutions falling short? What tactical shifts could help them reclaim share?

- What are the whitespace opportunities for Canadian financial institutions to adapt this playbook to their markets?

Who is RightMetric?

A strategic insights partner combining audience, content, and channel research to provide mission-critical intelligence to marketing strategists.

About Chime

Discover how Chime redefined what a bank could be by solving real problems with empathy. This chapter breaks down the foundation of Chime’s success: serving overlooked audiences with products that feel more like financial lifelines than features.

Founded in 2014, Chime is a US-based neobank that disrupted traditional financial services by offering a mobile-first, no-fee banking experience. Rather than targeting affluent urban professionals like most fintech upstarts, Chime leaned into underserved populations that included gig workers, newcomers, students, and service employees.

Chime has emerged as a leading disruptor, leveraging simple banking, strong mobile UX, and savvy digital marketing to outpace traditional competitors in key segments. It now serves over 22M1 consumers with annual growth of roughly 30% by solving money problems with digital ease and dignity.

Its meteoric rise reveals how the financial industry is being redefined not just by innovation, but by inclusion.

1 Report: Chime business breakdown & founding story: Contrary research. Report: Chime Business Breakdown & Founding Story | Contrary Research. (n.d.). https://research.contrary.com/company/chime

Chime’s growth was not driven by complex features but by emotionally resonant tools. It became a financial co-pilot for consumers who often felt excluded or penalized by legacy systems, acquiring a strong user base by addressing unmet needs.

New products will continue to erode traditional banks' share - eating more of the banking pie as Chime leverages its established customer trust and expands its offerings.

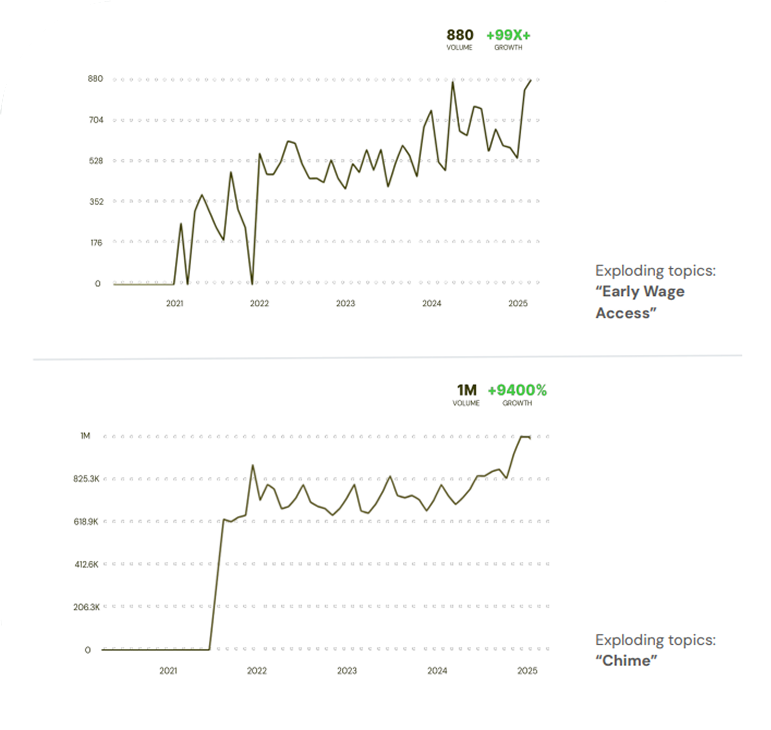

Chime has experienced explosive growth since 2021, a surge significantly influenced by the September 2019 launch of 'Spot Me'. This was a feature that ignited a broader cultural conversation around fee-free overdraft and Early Wage Access (EWA). Data indicates a sharp rise in search interest following its release, suggesting a mutual acceleration of awareness driven by Chime's rapid user growth.

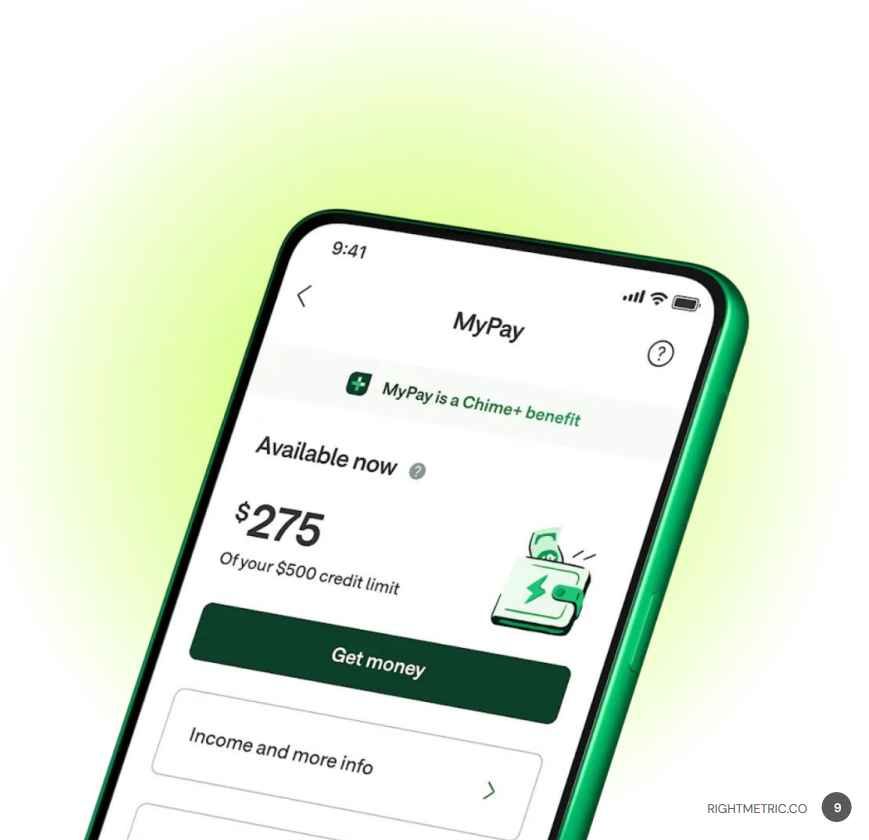

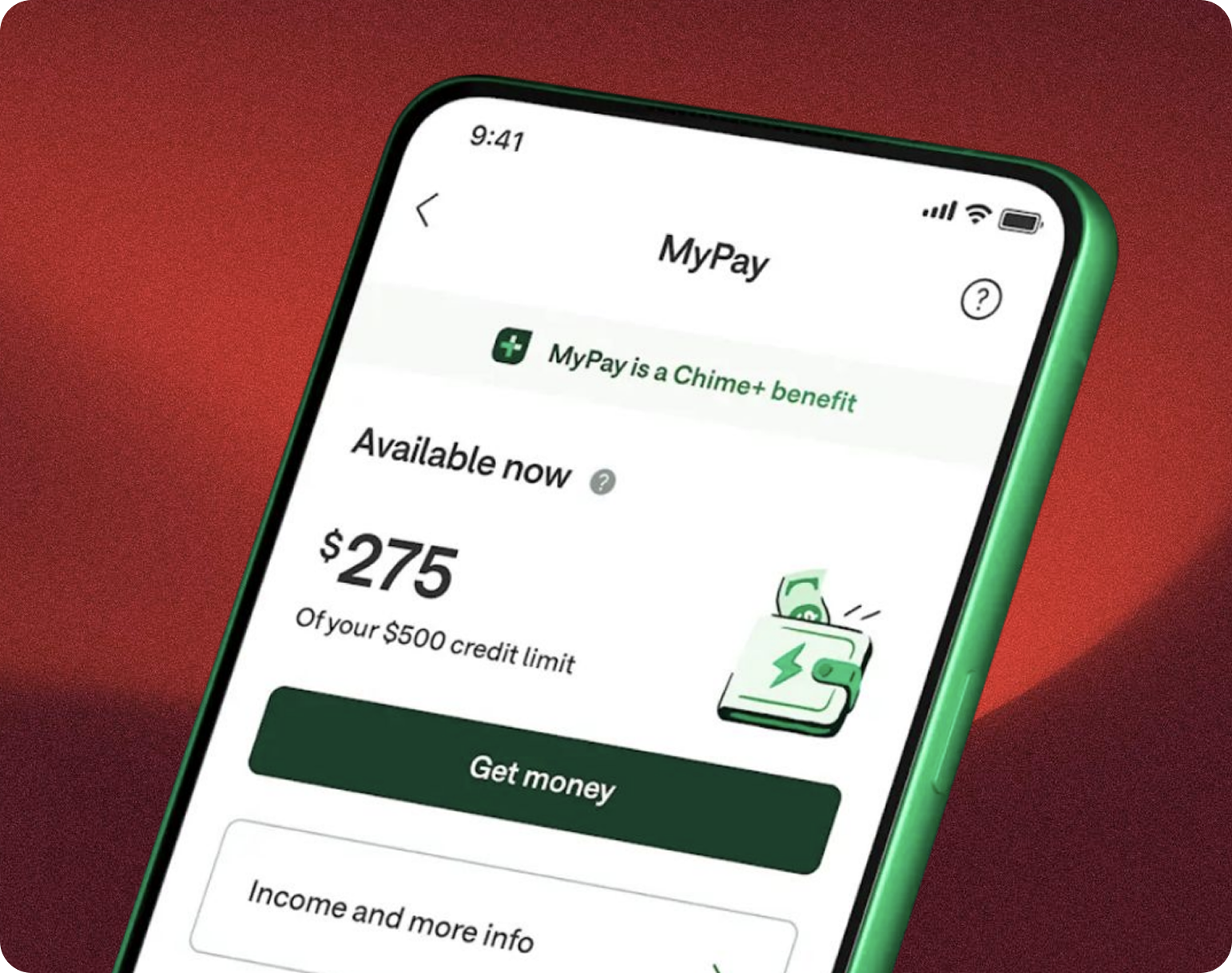

Fast forward to July 2024, with the rollout of “My Pay”, allowing consumers to access up to $500 ahead of payday, and we see yet another noticeable spike. This reinforces Chime’s position as more than just a follower of financial trends but a market mover, designing products/services to meet the unmet needs of consumers.

Search interest in “early wage access” has grown +9400% over five years, with volume topping 1 million monthly searches which is a clear signal that demand for financial flexibility isn’t a niche issue, it’s now a mainstream expectation.

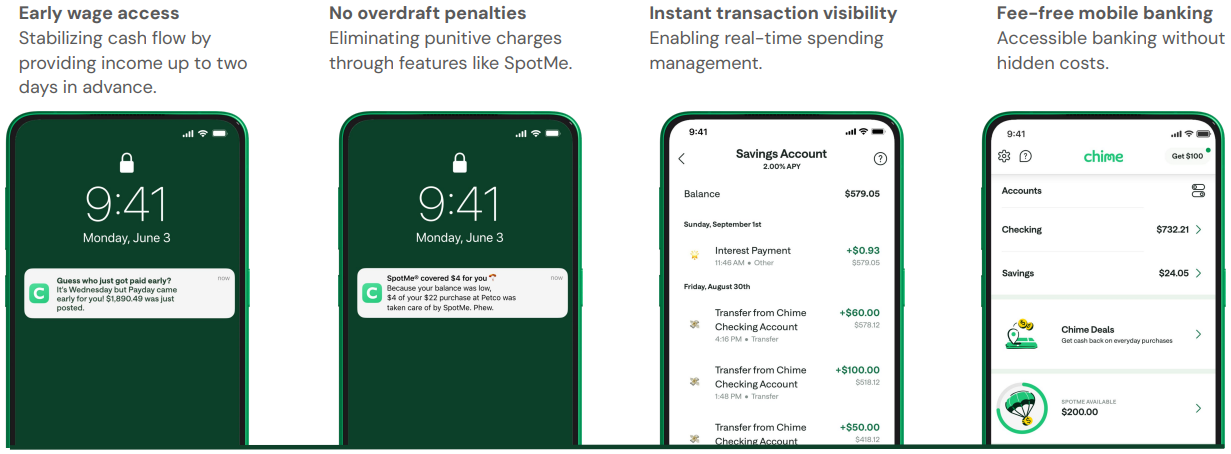

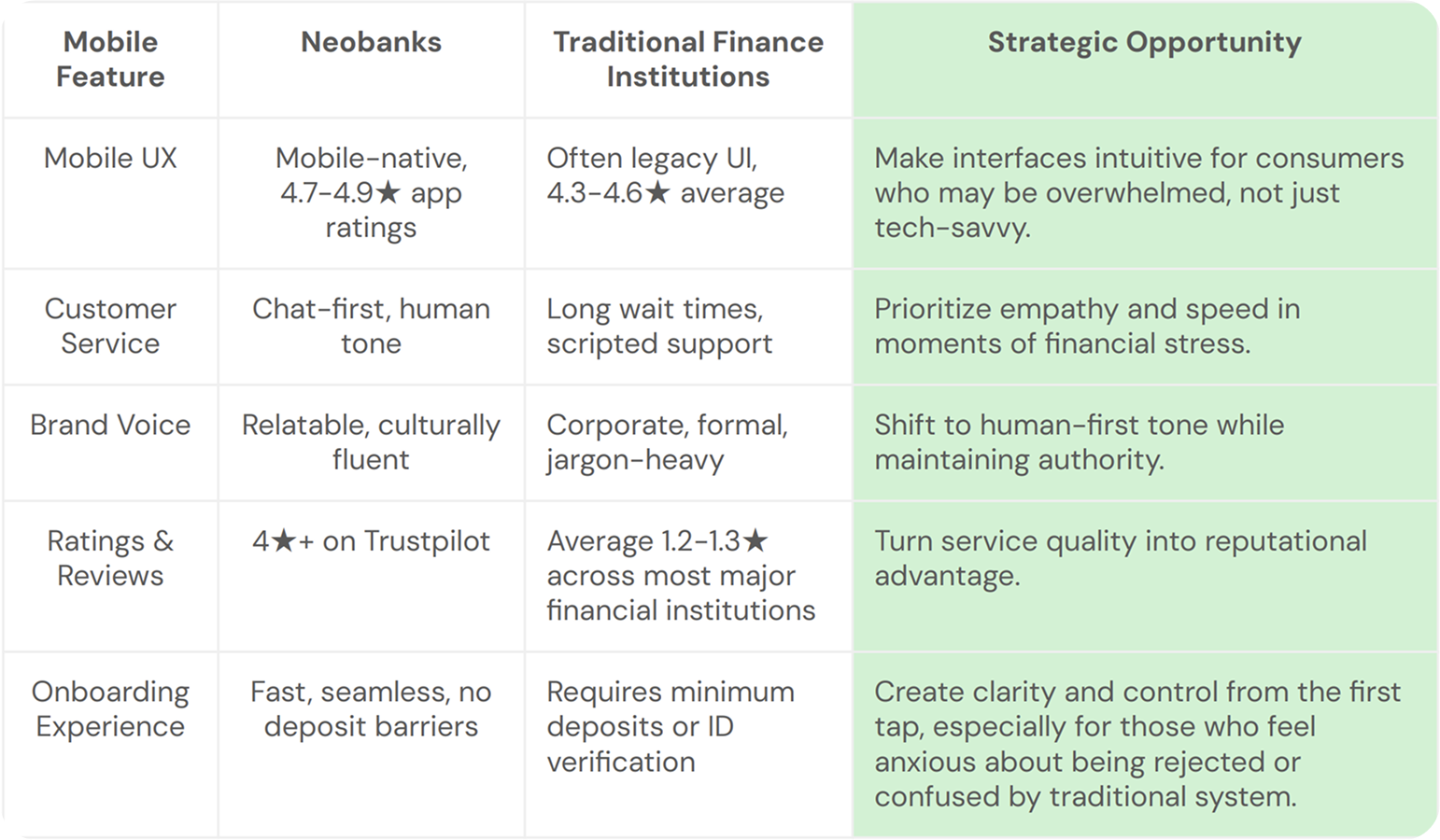

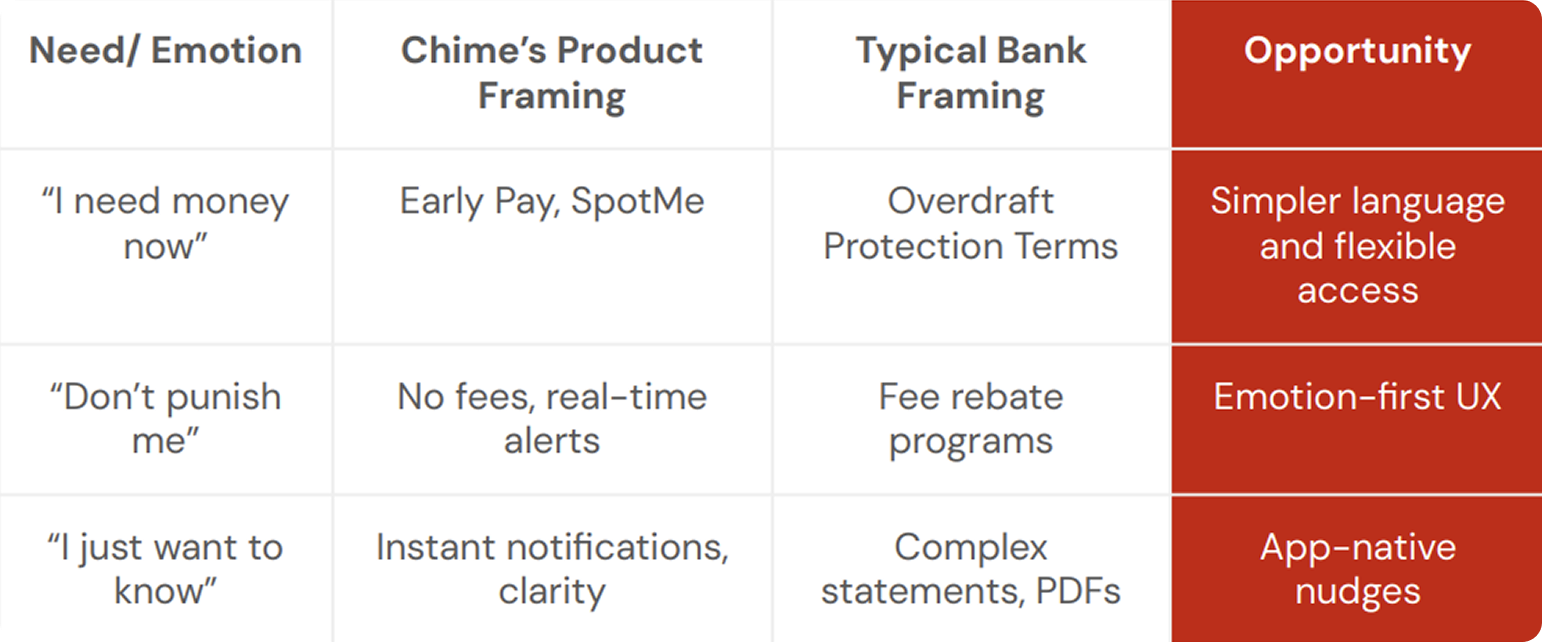

Chime effectively addressed these pain points by offering:

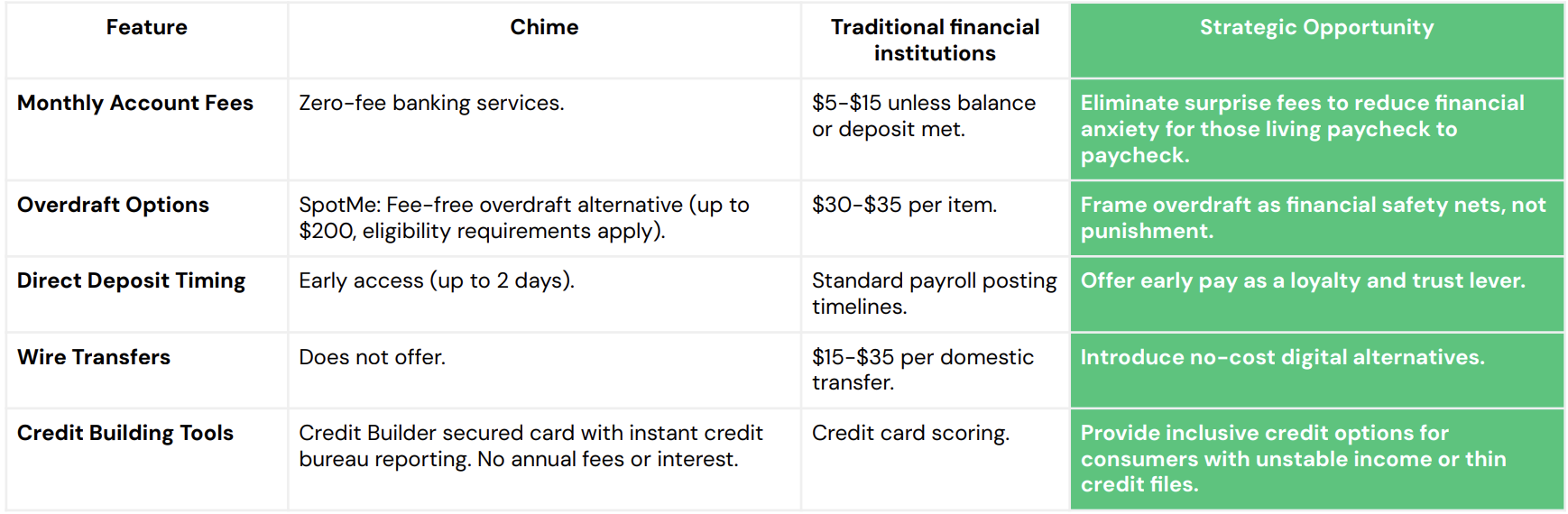

Service Comparison Table

Comparing Chime's services with traditional banks highlights the gaps in how traditional banking meets the needs of underserved customers

Chime removed shame, made things simpler, and built a user experience that made people feel in control. Traditional financial institutions may offer similar features, but without the emotional fluency Chime brings to the table, they often fall flat.

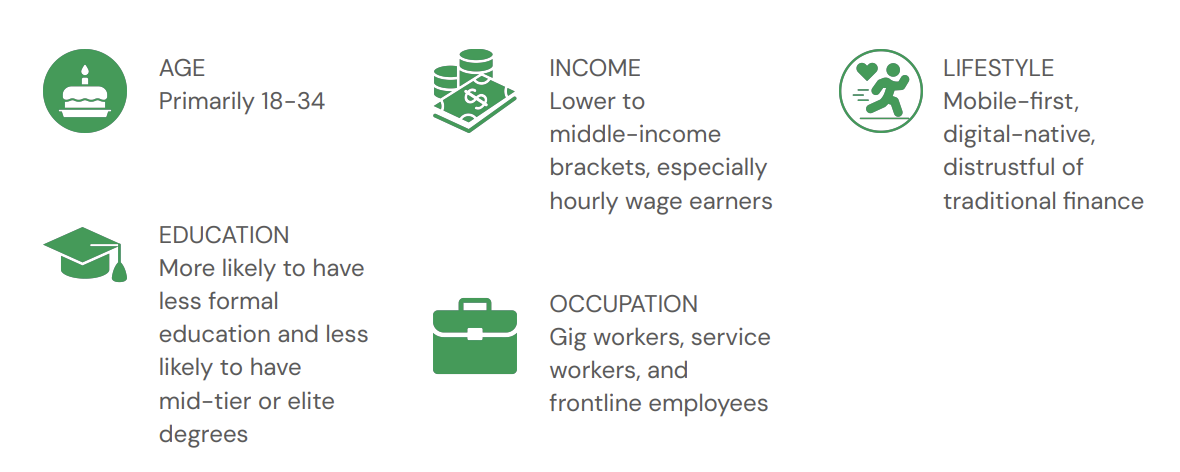

Chime’s Target Demographics

Chime’s success is rooted in understanding and then slightly subverting the typical neobank audience profile. While many digital banking challengers begin by chasing upwardly mobile urban professionals, Chime’s actual traction has been skewed toward a different user archetype:

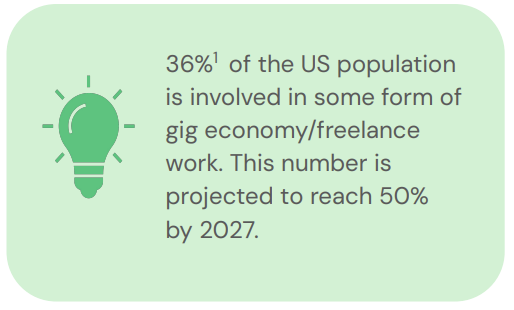

The Gig Economy Boom

The US gig economy, encompassing freelancers, ride-hailing drivers, delivery app contractors, and part-time creators, represents a significant portion of the workforce. They face challenges like income volatility, delayed payments, and limited access to credit.

For many gig workers, Chime’s solutions provide more than just convenience; they restore a sense of financial dignity. It acknowledges the unique challenges of gig economy work and delivers frictionless, inclusive solutions that legacy financial institutions often overlook.

While gig economy workers signal a shift in how people earn, the deeper trend is financial insufficiency and that reality cuts across jobs, ages, and income brackets. In the US, nearly half of Americans earning $50K or less say they’re falling behind.

Chime’s strategic intent has long been to appeal to an aspirational, tech-forward, financially curious base.

Our understanding of this audience comes from a multi-faceted approach, aiming to understand how they engage and build trust. By triangulating insights from Chime's app user base (both Android and iOS), analyzing web data through our tools, and observing social behaviours, clear patterns emerged. This holistic view helps us understand how Chime is effectively gamifying trust with its consumers.

Rather than dominating elite metros and highly educated consumers, Chime has carved out strength in communities overlooked by legacy financial institutions. These are consumers who value low fees, mobile access, and cash flow needs. Chime’s approach doesn’t just serve these consumers; it validates and humanizes them. It treats them as savvy money managers in their own right, creating a brand that says: “You’re not bad with money. The system was built against you.”

Chime’s success in the US was driven by targeting cities with high concentrations of underbanked and working-class populations. Chime, or a competitor that moves first, could apply this exact playbook to capture underserved Canadian audiences.

What this means for Canada: Landscape

The banking sector in Canada is stable but also stagnant. It’s dominated by a few major players, which has created high barriers to entry and limited innovation for underserved segments. As of spring 2024, 45% of Canadians are struggling to meet daily expenses due to rising prices1 , a 12% increase from two years ago. This number is expected to rise as gig work expands and the cost of living outpaces wage growth.

The demand for low-friction, empathy-first banking is not exclusive to the US, it’s growing quietly in Canada too. Traditional financial institutions that prioritize digital equity, flexible finance tools and straightforward UX have an opportunity to serve a growing audience that’s been historically underserved. To understand how Chime gained traction, we have to look at who they served first.

What this means for Canada: Gig Economy

Data suggests that roughly 7.3M1 Canadians engage in gig economy work, a trend that positions Chime to gain early traction by offering products tailored to their income patterns.

Canadian gig workers are also likely to face similar challenges as their US counterparts:

But the deeper insight is this: it’s not just gig workers feeling the pressure. Financial instability cuts across employment types, impacting full-time employees, service workers, and newcomers alike. Anyone struggling to keep up with life is part of Chime’s real addressable market.

This kind of broad, inclusive messaging is something Wealthsimple is actively leaning into, as seen in their candid, emotionally resonant campaign here. It stands in stark contrast to traditional financial institutions like RBC, whose “Ideas Happen Here” platform still leans on aspirational tropes like happy young families buying their first home, rather than meeting people where they actually are.

1 Behind the gig: Securian Canada Insights. (n.d.). https://www.securiancanada.ca/content/dam/doc/sc/securian-canada-gig-report-100824.pdf

What this means for Canada: Underserved

Beyond the gig economy, Chime is also likely to target other underserved segments in Canada:

First-Time Banking Customers

Newcomers to Canada and young adults often find themselves excluded from traditional banking due to identification requirements, complex applications, or minimum balance stipulations. High monthly fees and inaccessible interfaces add to the barriers.

These consumers need accounts that are simple to open, mobile-friendly, and transparent in their fee structure. A mobile app with clear onboarding, educational nudges, and smart saving tips can turn financial friction into trust and loyalty.

Students

Students typically manage fluctuating finances like grants, part-time wages, tuition expenses and lack the time or financial literacy to optimize complex financial products. Most are not ready for investment platforms or long-term saving strategies. They just want to avoid overdrafts and budget for groceries.

Chime’s approach to no-fee banking, combined with its easy-to-use app and budgeting tools, aligns perfectly with this lifestyle. In Canada, students remain a largely under-optimized audience segment.

Other Underserved Niches

- New immigrants with no local credit history are often rejected or given inferior banking products.

- Remote Indigenous communities face geographic barriers and limited access to physical branches or reliable WiFi and cell service.

- Service industry workers particularly in tourism, agriculture, hospitality, and retail operate on unstable income and need flexible tools to manage unpredictable pay cycles.

What this means for Canada: Strategy

Chime would likely pursue these underserved communities early on in its Canadian expansion, bringing mobile-first, no-fee products that align with their needs.

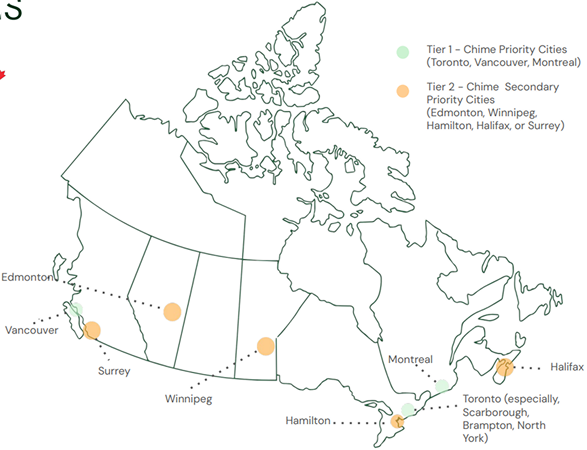

1. Don’t assume Chime will only go for big cities first. While Chime may launch with campaigns focused on Toronto, Vancouver, or Montreal, their traction could arise from: Edmonton, Winnipeg, Hamilton, Surrey, Halifax, Atlantic Canada or remote Northern Ontario.

2. Expect Chime to overperform where bank infrastructure is weak. Regions with high underbanked populations may quickly adopt Chime’s low-friction model. 3. Preempt the underserve

3. Preempt the underserved opportunity by launching digital-first outreach and products in smaller urban hubs, gig-heavy communities, and multicultural districts with high newcomer density.

4. Embrace digital equity. Your next wave of customers want no-fee structures, early pay or pay smoothing tools, and built-in trust through accessible onboarding, plain language, and mobile-first support.

These user segments aren’t niche anymore but the new mainstream. Yet many still encounter surprise fees, rigid requirements, or broken access to funds. Neobanks like Chime have gained traction not just by noticing these tensions but by removing them.

What this means for Canada: Priority Cities

We can expect Chime to prioritize urban centres with growing working-class and gig economy consumers. While Tier 1 cities will be on the radar, Chime’s US experience suggests its purpose-built products may gain faster in Tier 2 markets.

Chime’s Growth Engine

The strategies behind Chime’s meteoric rise. This chapter reveals how simplicity, mobile-first UX, and culturally fluent marketing turned a challenger brand into a household name, especially for those traditionally left behind by big banks.

Chime’s Value Proposition

Chime’s brand strategy is rooted in designing financial tools for the historically underserved. Their success hinges on offering a banking experience that feels intuitive, frictionless, and fair, particularly to consumers frustrated by the fees and complexity of traditional financial institutions.

1 Based on a custom-built dataset of hundreds of scraped online mentions of Chime (articles, blogs, web content). These mentions were analysed for sentiment and the specific product/feature being discussed.

The three most frequently highlighted features across Chime’s digital advertising reflect this core:

- Low/No Fees - Transparent, fee-free banking with no overdraft, minimum balance, or account maintenance charges.

Executive Summary

Chime didn't win by building a better bank. It won by building a more relatable one. Its meteoric rise in the US banking landscape wasn’t just about a better digital experience but a strategic mix of audience-first products, creator-powered storytelling, and platform-native brand behaviour. Chime’s growth is built on meeting the needs of a much broader reality, reaching millions of consumers who feel financially precarious or excluded by traditional systems.

We analysed our datasets to uncover trends which we translated into actionable recommendations for financial services marketers and leaders.

In a rush? Skip to the end for our 90-180 day action plan.

Key takeaways

- Chime’s real audience isn’t who you think. While positioned as a solution for tech-savvy urbanites, Chime over-indexes in overlooked cities and underserved communities. It built a banking experience not just for consumers but with them.

- Social fluency is Chime’s moat. Chime thrives where culture happens: TikTok, Reddit, Snapchat, by not just showing up but by sounding native. It speaks the language of its consumers, not the language of lenders, building emotional relevance faster than traditional financial institutions’ polished campaigns.

- Chime operationalized empathy. Every feature - early pay, no fees, real-time notifications - solves a real pain point. The magic isn’t complexity. It’s clarity, dignity, and frictionless design.

- Canada is next. Chime may have started in the US, but the conditions driving its rise – financial anxiety & a distrust in traditional finance – are playing out globally

The questions we answered

In 2025, the financial landscape is undergoing a rapid transformation, driven by disruptors like Chime. This report delves into Chime's growth engine and its challenge to traditional banking models, examining how it has shifted industry dynamics, reshaped audience expectations, and created a unique playbook.

To provide actionable insights for financial institutions navigating this change, we answer the following questions:

- How is Chime’s rapid growth redefining the financial landscape, and what can financial institutions learn from its playbook to stay competitive?

- What consumer segment is Chime serving most effectively, and why does this audience matter?

- How has Chime tailored its products, positioning, and content to resonate with the underbanked?

- What content strategies and creative themes drive adoption and trust with Chime’s audience?

- Which social and digital platforms are most effective for Chime, and how do these choices differ from traditional financial brands?

- What brand partnerships, creators, and media strategies have powered Chime’s growth?

- Where are traditional financial institutions falling short? What tactical shifts could help them reclaim share?

- What are the whitespace opportunities for Canadian financial institutions to adapt this playbook to their markets?

How this report was created

This report was created by RightMetric’s expert research team, who looked deep into our datasets by leveraging over 25+ powerful data gathering tools. By weaving together various digital data points,, including audience demographics, behaviour, engagement metrics, and advertising campaigns, we are able to spot trends and opportunities.

We then employed proprietary methodologies to refine raw data and craft reports that tell the full story, delivering clear and actionable insights.

- How is Chime’s rapid growth redefining the financial landscape, and what can financial institutions learn from its playbook to stay competitive?

- What consumer segment is Chime serving most effectively, and why does this audience matter?

- How has Chime tailored its products, positioning, and content to resonate with the underbanked?

- What content strategies and creative themes drive adoption and trust with Chime’s audience?

- Which social and digital platforms are most effective for Chime, and how do these choices differ from traditional financial brands?

- What brand partnerships, creators, and media strategies have powered Chime’s growth?

- Where are traditional financial institutions falling short? What tactical shifts could help them reclaim share?

- What are the whitespace opportunities for Canadian financial institutions to adapt this playbook to their markets?

Who is RightMetric?

A strategic insights partner combining audience, content, and channel research to provide mission-critical intelligence to marketing strategists.

About Chime

Discover how Chime redefined what a bank could be by solving real problems with empathy. This chapter breaks down the foundation of Chime’s success: serving overlooked audiences with products that feel more like financial lifelines than features.

Founded in 2014, Chime is a US-based neobank that disrupted traditional financial services by offering a mobile-first, no-fee banking experience. Rather than targeting affluent urban professionals like most fintech upstarts, Chime leaned into underserved populations that included gig workers, newcomers, students, and service employees.

Chime has emerged as a leading disruptor, leveraging simple banking, strong mobile UX, and savvy digital marketing to outpace traditional competitors in key segments. It now serves over 22M1 consumers with annual growth of roughly 30% by solving money problems with digital ease and dignity.

Its meteoric rise reveals how the financial industry is being redefined not just by innovation, but by inclusion.

1 Report: Chime business breakdown & founding story: Contrary research. Report: Chime Business Breakdown & Founding Story | Contrary Research. (n.d.). https://research.contrary.com/company/chime

Chime’s growth was not driven by complex features but by emotionally resonant tools. It became a financial co-pilot for consumers who often felt excluded or penalized by legacy systems, acquiring a strong user base by addressing unmet needs.

New products will continue to erode traditional banks' share - eating more of the banking pie as Chime leverages its established customer trust and expands its offerings.

Chime has experienced explosive growth since 2021, a surge significantly influenced by the September 2019 launch of 'Spot Me'. This was a feature that ignited a broader cultural conversation around fee-free overdraft and Early Wage Access (EWA). Data indicates a sharp rise in search interest following its release, suggesting a mutual acceleration of awareness driven by Chime's rapid user growth.

Fast forward to July 2024, with the rollout of “My Pay”, allowing consumers to access up to $500 ahead of payday, and we see yet another noticeable spike. This reinforces Chime’s position as more than just a follower of financial trends but a market mover, designing products/services to meet the unmet needs of consumers.

Search interest in “early wage access” has grown +9400% over five years, with volume topping 1 million monthly searches which is a clear signal that demand for financial flexibility isn’t a niche issue, it’s now a mainstream expectation.

Chime effectively addressed these pain points by offering:

Service Comparison Table

Comparing Chime's services with traditional banks highlights the gaps in how traditional banking meets the needs of underserved customers

Chime removed shame, made things simpler, and built a user experience that made people feel in control. Traditional financial institutions may offer similar features, but without the emotional fluency Chime brings to the table, they often fall flat.

Chime’s Target Demographics

Chime’s success is rooted in understanding and then slightly subverting the typical neobank audience profile. While many digital banking challengers begin by chasing upwardly mobile urban professionals, Chime’s actual traction has been skewed toward a different user archetype:

The Gig Economy Boom

The US gig economy, encompassing freelancers, ride-hailing drivers, delivery app contractors, and part-time creators, represents a significant portion of the workforce. They face challenges like income volatility, delayed payments, and limited access to credit.

For many gig workers, Chime’s solutions provide more than just convenience; they restore a sense of financial dignity. It acknowledges the unique challenges of gig economy work and delivers frictionless, inclusive solutions that legacy financial institutions often overlook.

While gig economy workers signal a shift in how people earn, the deeper trend is financial insufficiency and that reality cuts across jobs, ages, and income brackets. In the US, nearly half of Americans earning $50K or less say they’re falling behind.

Chime’s strategic intent has long been to appeal to an aspirational, tech-forward, financially curious base.

Our understanding of this audience comes from a multi-faceted approach, aiming to understand how they engage and build trust. By triangulating insights from Chime's app user base (both Android and iOS), analyzing web data through our tools, and observing social behaviours, clear patterns emerged. This holistic view helps us understand how Chime is effectively gamifying trust with its consumers.

Rather than dominating elite metros and highly educated consumers, Chime has carved out strength in communities overlooked by legacy financial institutions. These are consumers who value low fees, mobile access, and cash flow needs. Chime’s approach doesn’t just serve these consumers; it validates and humanizes them. It treats them as savvy money managers in their own right, creating a brand that says: “You’re not bad with money. The system was built against you.”

Chime’s success in the US was driven by targeting cities with high concentrations of underbanked and working-class populations. Chime, or a competitor that moves first, could apply this exact playbook to capture underserved Canadian audiences.

What this means for Canada: Landscape

The banking sector in Canada is stable but also stagnant. It’s dominated by a few major players, which has created high barriers to entry and limited innovation for underserved segments. As of spring 2024, 45% of Canadians are struggling to meet daily expenses due to rising prices1 , a 12% increase from two years ago. This number is expected to rise as gig work expands and the cost of living outpaces wage growth.

The demand for low-friction, empathy-first banking is not exclusive to the US, it’s growing quietly in Canada too. Traditional financial institutions that prioritize digital equity, flexible finance tools and straightforward UX have an opportunity to serve a growing audience that’s been historically underserved. To understand how Chime gained traction, we have to look at who they served first.

What this means for Canada: Gig Economy

Data suggests that roughly 7.3M1 Canadians engage in gig economy work, a trend that positions Chime to gain early traction by offering products tailored to their income patterns.

Canadian gig workers are also likely to face similar challenges as their US counterparts:

But the deeper insight is this: it’s not just gig workers feeling the pressure. Financial instability cuts across employment types, impacting full-time employees, service workers, and newcomers alike. Anyone struggling to keep up with life is part of Chime’s real addressable market.

This kind of broad, inclusive messaging is something Wealthsimple is actively leaning into, as seen in their candid, emotionally resonant campaign here. It stands in stark contrast to traditional financial institutions like RBC, whose “Ideas Happen Here” platform still leans on aspirational tropes like happy young families buying their first home, rather than meeting people where they actually are.

1 Behind the gig: Securian Canada Insights. (n.d.). https://www.securiancanada.ca/content/dam/doc/sc/securian-canada-gig-report-100824.pdf

What this means for Canada: Underserved

Beyond the gig economy, Chime is also likely to target other underserved segments in Canada:

First-Time Banking Customers

Newcomers to Canada and young adults often find themselves excluded from traditional banking due to identification requirements, complex applications, or minimum balance stipulations. High monthly fees and inaccessible interfaces add to the barriers.

These consumers need accounts that are simple to open, mobile-friendly, and transparent in their fee structure. A mobile app with clear onboarding, educational nudges, and smart saving tips can turn financial friction into trust and loyalty.

Students

Students typically manage fluctuating finances like grants, part-time wages, tuition expenses and lack the time or financial literacy to optimize complex financial products. Most are not ready for investment platforms or long-term saving strategies. They just want to avoid overdrafts and budget for groceries.

Chime’s approach to no-fee banking, combined with its easy-to-use app and budgeting tools, aligns perfectly with this lifestyle. In Canada, students remain a largely under-optimized audience segment.

Other Underserved Niches

- New immigrants with no local credit history are often rejected or given inferior banking products.

- Remote Indigenous communities face geographic barriers and limited access to physical branches or reliable WiFi and cell service.

- Service industry workers particularly in tourism, agriculture, hospitality, and retail operate on unstable income and need flexible tools to manage unpredictable pay cycles.

What this means for Canada: Strategy

Chime would likely pursue these underserved communities early on in its Canadian expansion, bringing mobile-first, no-fee products that align with their needs.

1. Don’t assume Chime will only go for big cities first. While Chime may launch with campaigns focused on Toronto, Vancouver, or Montreal, their traction could arise from: Edmonton, Winnipeg, Hamilton, Surrey, Halifax, Atlantic Canada or remote Northern Ontario.

2. Expect Chime to overperform where bank infrastructure is weak. Regions with high underbanked populations may quickly adopt Chime’s low-friction model. 3. Preempt the underserve

3. Preempt the underserved opportunity by launching digital-first outreach and products in smaller urban hubs, gig-heavy communities, and multicultural districts with high newcomer density.

4. Embrace digital equity. Your next wave of customers want no-fee structures, early pay or pay smoothing tools, and built-in trust through accessible onboarding, plain language, and mobile-first support.

These user segments aren’t niche anymore but the new mainstream. Yet many still encounter surprise fees, rigid requirements, or broken access to funds. Neobanks like Chime have gained traction not just by noticing these tensions but by removing them.

What this means for Canada: Priority Cities

We can expect Chime to prioritize urban centres with growing working-class and gig economy consumers. While Tier 1 cities will be on the radar, Chime’s US experience suggests its purpose-built products may gain faster in Tier 2 markets.

Chime’s Growth Engine

The strategies behind Chime’s meteoric rise. This chapter reveals how simplicity, mobile-first UX, and culturally fluent marketing turned a challenger brand into a household name, especially for those traditionally left behind by big banks.

Chime’s Value Proposition

Chime’s brand strategy is rooted in designing financial tools for the historically underserved. Their success hinges on offering a banking experience that feels intuitive, frictionless, and fair, particularly to consumers frustrated by the fees and complexity of traditional financial institutions.

1 Based on a custom-built dataset of hundreds of scraped online mentions of Chime (articles, blogs, web content). These mentions were analysed for sentiment and the specific product/feature being discussed.

The three most frequently highlighted features across Chime’s digital advertising reflect this core:

- Low/No Fees - Transparent, fee-free banking with no overdraft, minimum balance, or account maintenance charges.

- Early pay with SpotMe - Access up to $200 in advance via early direct deposit and overdraft coverage.

- Intuitive Mobile App - Real-time notifications, easy-to-use budgeting tools, and interface simplicity.

Chime’s Voice & Vibe

Chime isn’t designing for an idealized version of the user - someone who pays bills on time, financially literate, perfectly organized. Instead, it’s designing for how people actually live:

- Unpredictable pay

- Low balances

- Emotional spending

- Financial anxiety

- Learning on the go

- Managing money while tired, busy, or overwhelmed

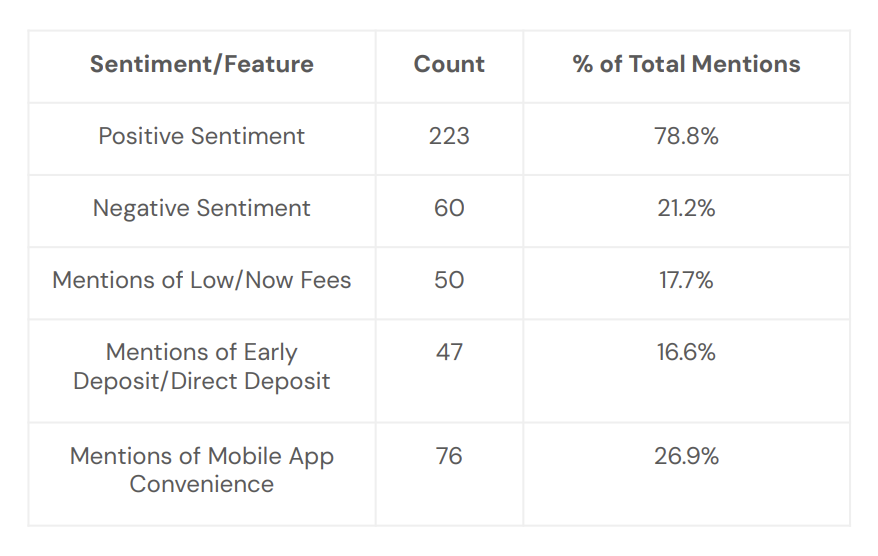

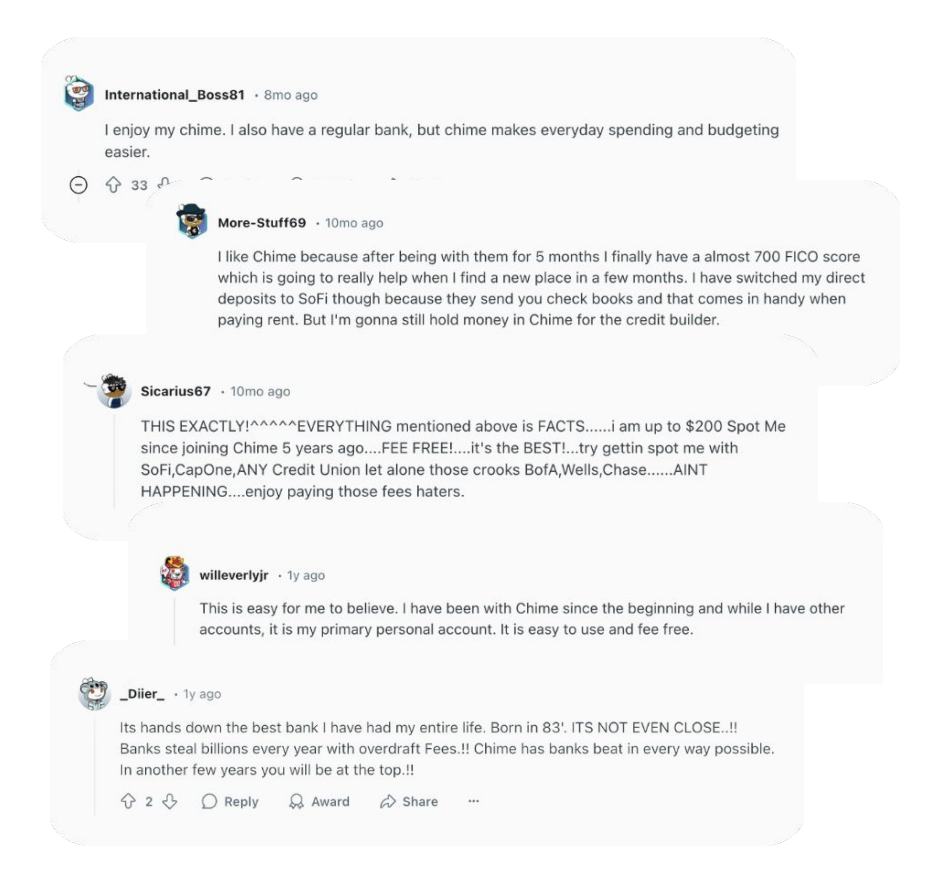

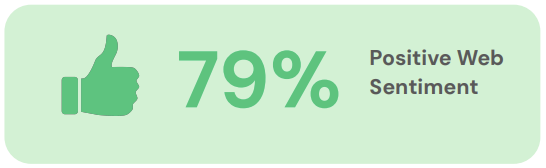

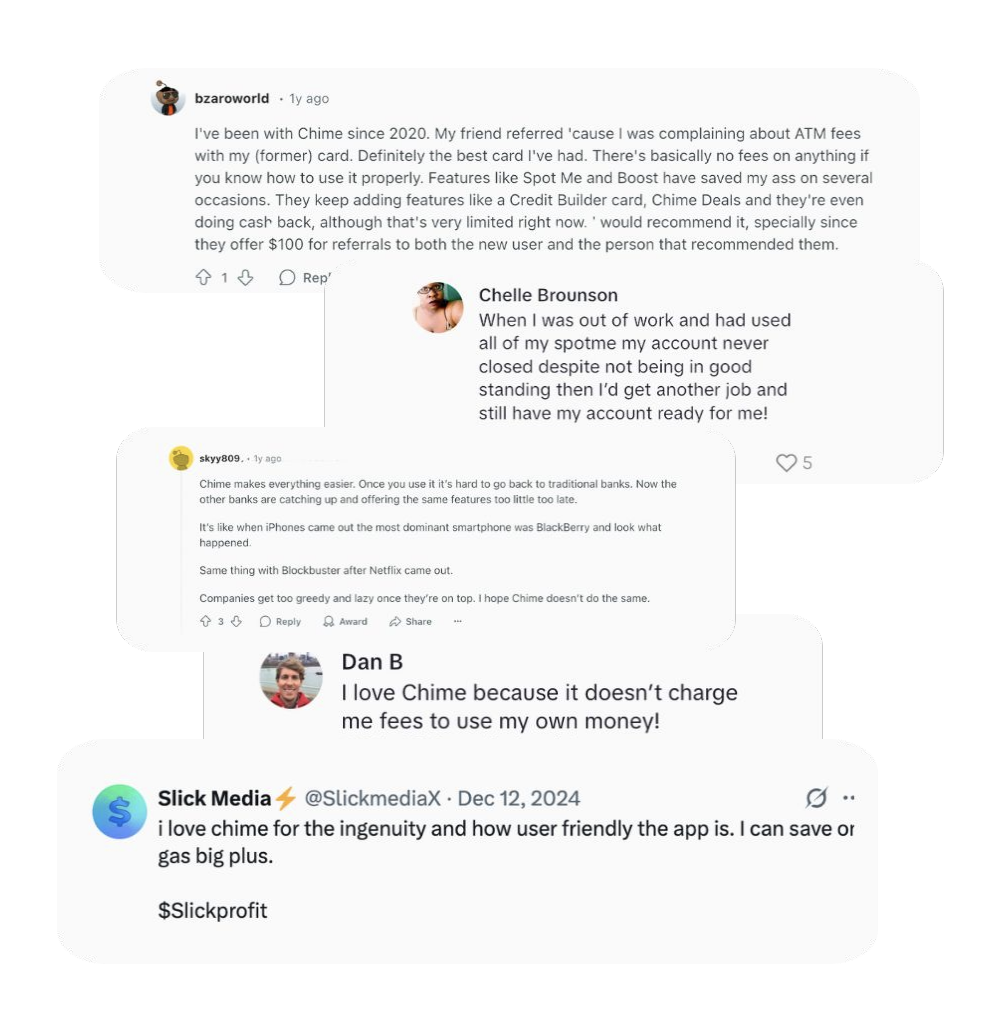

Chime’s Brand Sentiment

Our web sentiment1 analysis of Chime shows that 79% of online brand conversation is positive – an unusually high rate for a financial brand.

1 To arrive at Chime's 79% positive web sentiment score, we conducted a thorough content analysis of over 280 articles from financial news, blogs, and review sites over the past year. Each mention was manually tagged as positive or negative, and we simultaneously tracked mentions of key features like low fees, early payday, and app convenience. This analysis was further supported by evaluating thousands of social media posts and user reviews on platforms like TikTok and Reddit to understand emotional resonance. This multi-layered approach links positive sentiment directly to Chime's core value propositions of ease, affordability, and mobile-first banking

The top recurring brand differentiators driving this positive sentiment include mentions of:

- Low/no fees

- Early deposit/Direct deposit

- Mobile app convenience

These aren’t abstract benefits, these are survival-based use cases that resonate deeply with financially vulnerable consumers.

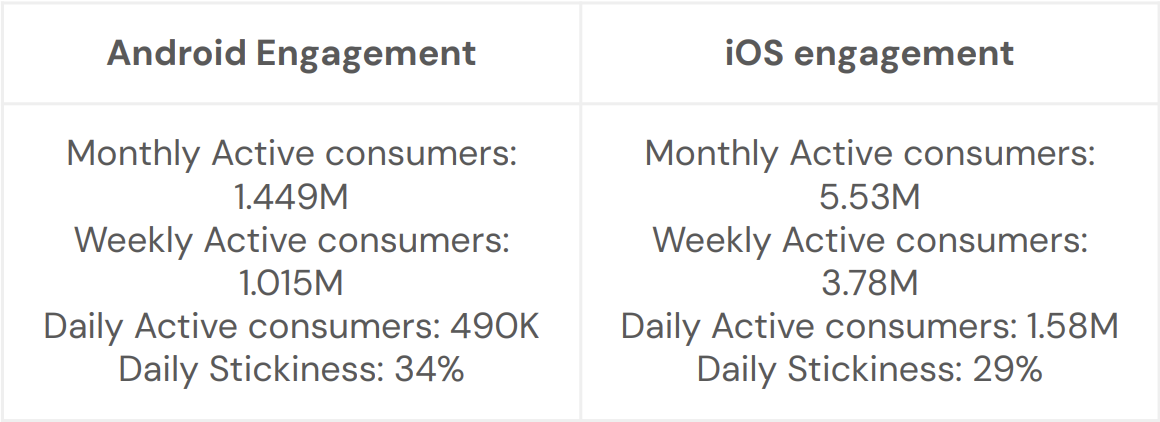

Chime’s App Engagement & UX

t’s not just the product but how it feels to use it. Dive into Chime’s app experience and see why their frictionless design and emotional clarity drive unusually high engagement and loyalty in a space where drop-off is the norm.

Engagement by Platform

What makes consumers stay with Chime isn’t just zero fees but how the brand makes them feel. This is how they create emotional utility. The following slide explores opportunities for traditional financial institutions, inspired by Chime's approach.

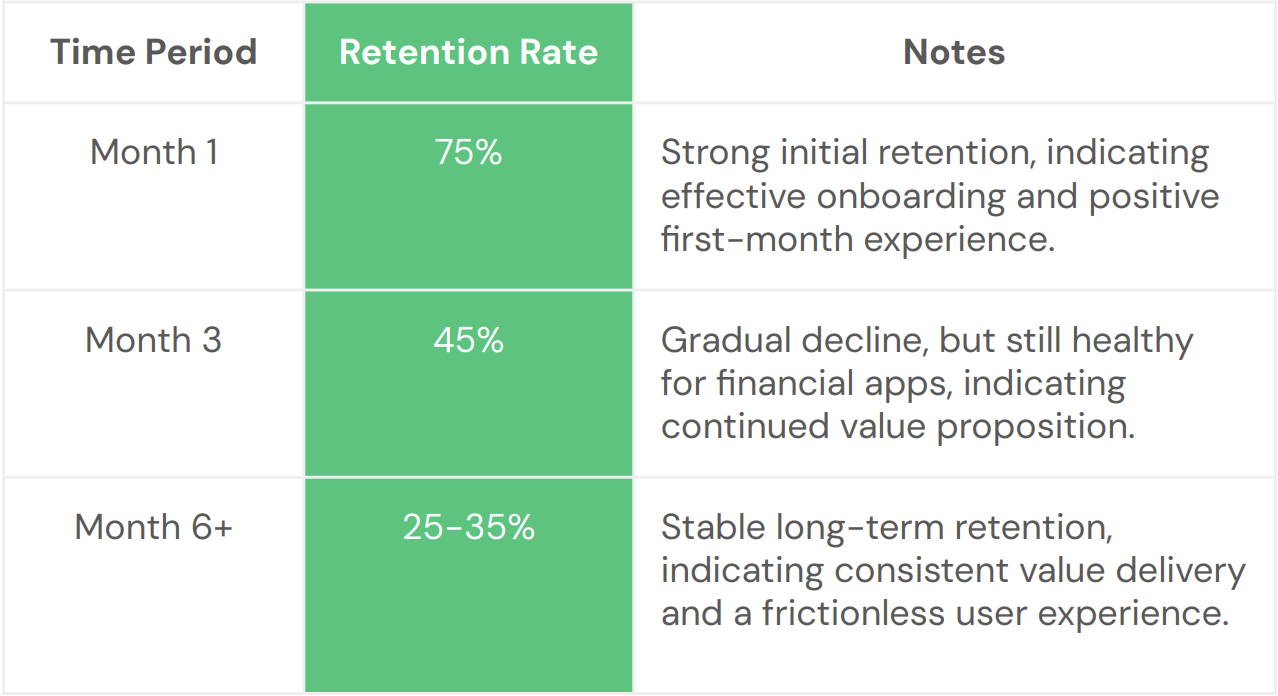

Retention Rates

1 Engagement and retention rates across Android and iOS were captured using Similarweb's App Analysis feature.

Chime’s UX, Brand Trust & Emotional Utility

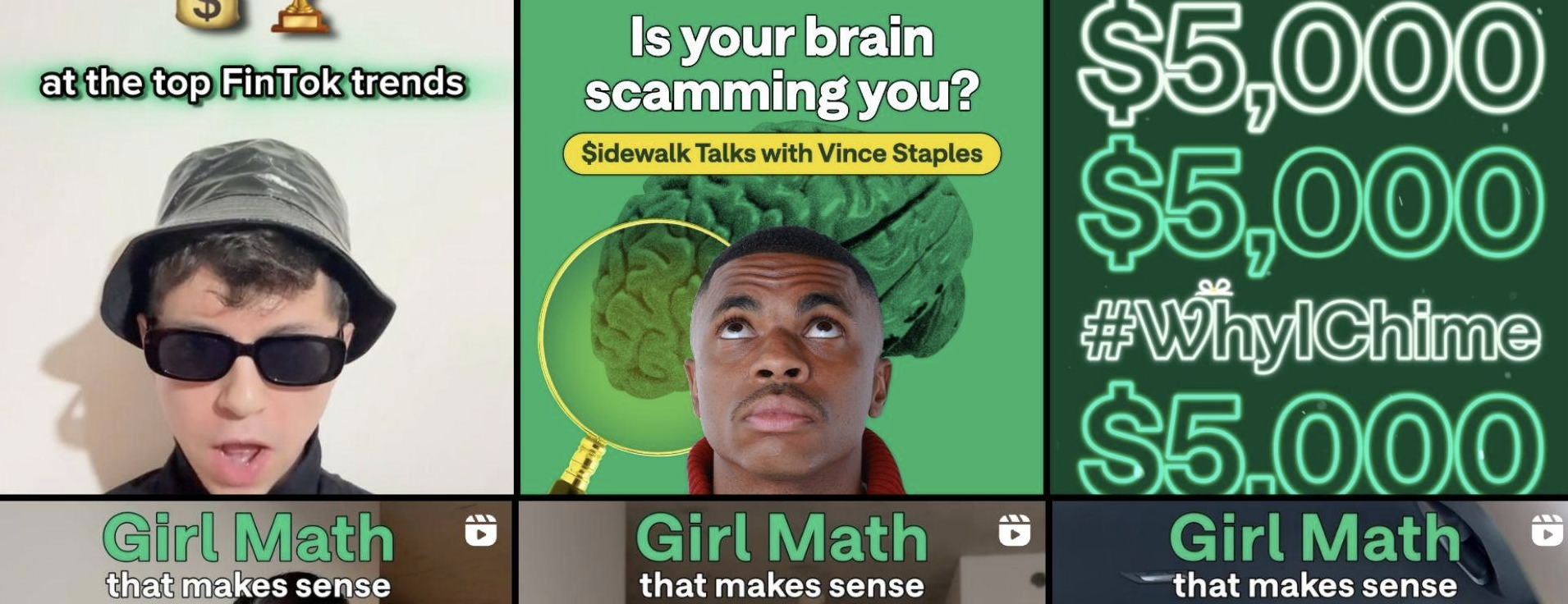

Chime’s Content Playbook

Step inside Chime’s creative strategy and see how they make finance feel human. From meme-driven TikToks to creator collabs, this chapter shows how storytelling, not just selling, builds trust with financially anxious audiences.

How Chime appeals to real people with real financial needs

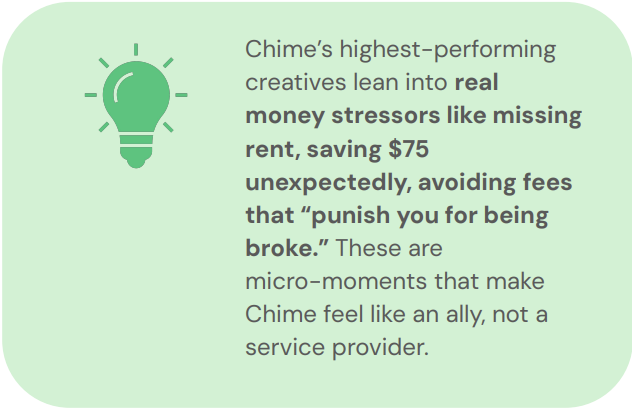

Chime doesn’t act like a bank. It acts like a mission-driven lifestyle brand. It focuses on relatable, emotional stories, especially in high-need areas. It’s brand resonates with consumers tired of being punished for being poor.

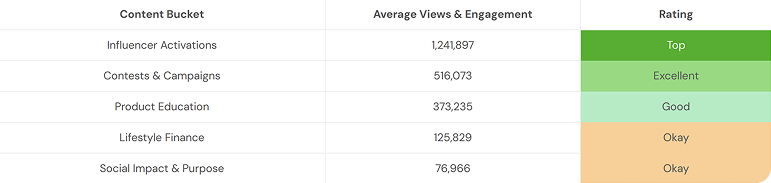

Chime’s top performing content buckets

One of Chime’s most successful tactics is its use of influencer activations. This was its strongest-performing organic content bucket1 in the US. Influencers created stories around getting paid early, avoiding fees, and rebuilding credit, with each tied to real financial pain points.

Lower performing buckets included: Sports & Athlete Partnerships, Behind-the-Scenes & Team Culture, Entertainment & Humor, Customer Love & Community, and Timely & Topical Content.

1 Our methodology for evaluating Chime's influencer partnerships combined quantitative engagement analysis with qualitative content assessment. We first analysed views and engagement metrics on TikTok, Instagram, and YouTube to identify high-performing "viral outliers." These were then subjected to qualitative analysis, involving manual review of thousands of audience comments for sentiment and an evaluation of content context (influencer style, tone, and thematic relevance). This two-pronged approach allowed us to move beyond simple metrics and understand why specific influencer content resonated authentically with audiences, linking engagement success to genuine creator alignment and messaging.

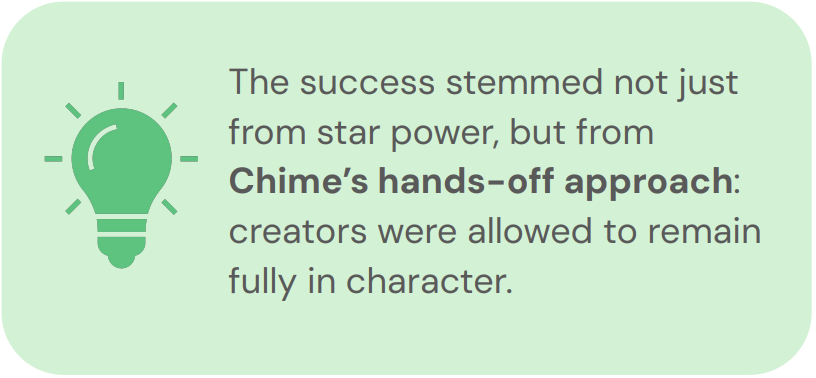

Standout Actvation: Kai Cenat and Fanum

Chime’s creator partnership with Kai Cenat and Fanum was both high-reach and high-resonance. The collaboration was for a content series to unveil MyPay, Chime’s new product that helps its customers “break free from the rigid pay schedule.” The campaign began with cryptic, branded teases during live streams, sparking speculation across TikTok, Twitch, and Instagram. It culminated in a real-world activation: a surprise money truck stunt in NYC, where the creators handed out Chime-branded rewards to fans.

* Views and engagement estimate (Mar 2024 - Feb 2025). Subject to data tool variations.

Streaming to a live audience of hundreds of thousands, the content was messy, hilarious, and unapologetically human. And that’s the lesson: financial institutions often prioritize control and compliance over cultural connection.

But today’s consumers want brands that show up in their world, not just peddle polished campaigns.

Product Education Through Culture: Vince Staples Campaign

Chime also launched a financial literacy series with rapper Vince Staples, including a segment called “Sidewalk Talk” that explores how pay cycles evolved and how MyPay offered a smarter, faster alternative.

* Views and engagement estimate (Mar 2024 - Feb 2025). Subject to data tool variations.

Another standout included a two-part collaboration with Reesa Teesa, where she broke down common money red flags in relationships. These weren’t dry explainers – they were jokes, stories, and culture-rich education pieces that consumers actually shared.

Ball on a Budget

Chime blurred the line between advertising and advice, especially on platforms like:

- Tiktok & Instagram Reels - Skits, side-by-side comparisons, and creator-led “edutainment” stories.

- YouTube - Longer testimonials and deep dives into Chime’s features.

- Facebook - Retargeting ads, user reviews, and casual financial education.

Chime’s Platform Strategy

Step inside Chime’s creative strategy and see how they make finance feel human. From meme-driven TikToks to creator collabs, this chapter shows how storytelling, not just selling, builds trust with financially anxious audiences.

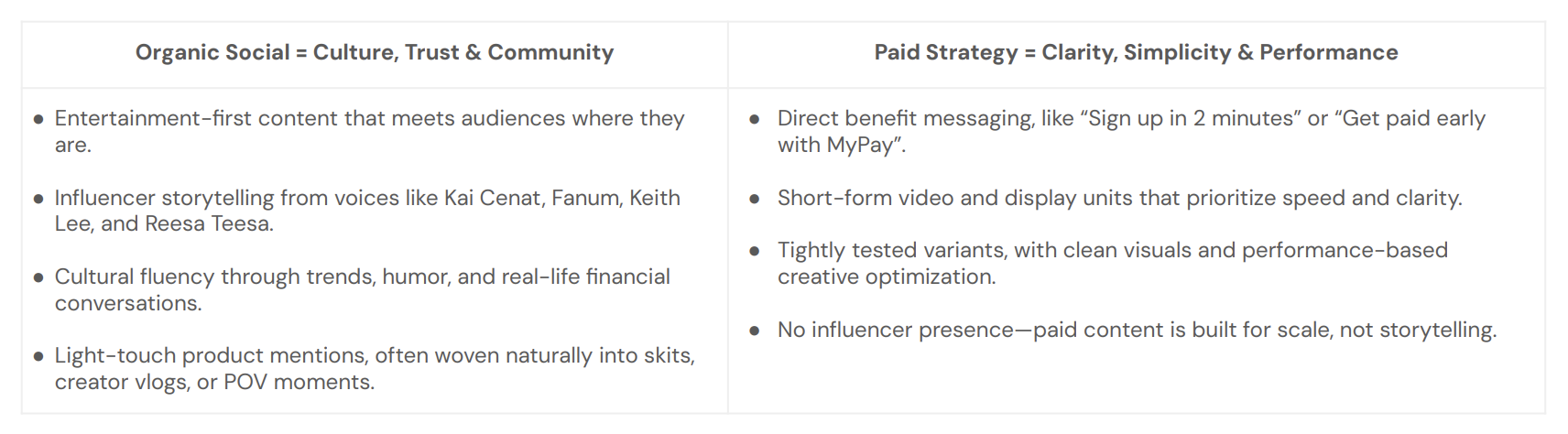

Chime’s Platform Strategy Organic vs Paid

Chime’s organic and paid strategies are distinct by design, each playing a unique role in the customer journey. While they don’t overlap in execution (e.g. influencer content is not repurposed in paid), both are critical levers in building brand momentum and performance.

RightMetric analysed over 200 videos across Chime’s social platforms (Instagram, TikTok, Facebook, LinkedIn), categorizing them by content type and assessing performance based on engagement metrics and editing styles. We then compared these findings to Chime’s paid media content to uncover strategic differences.

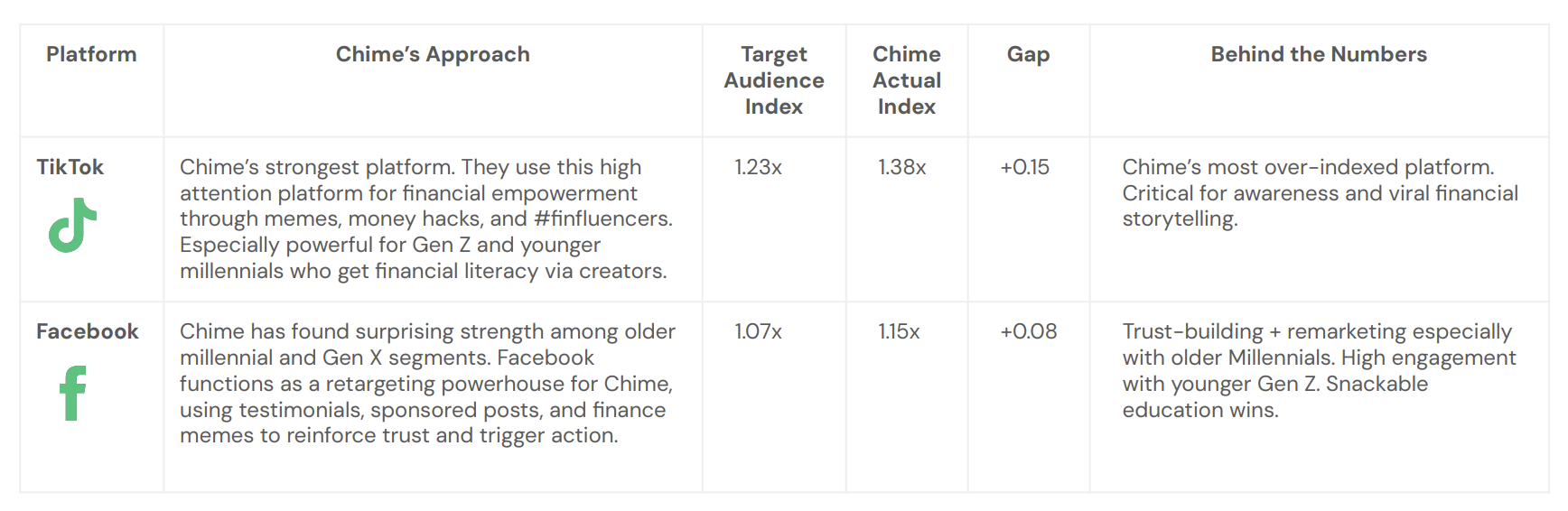

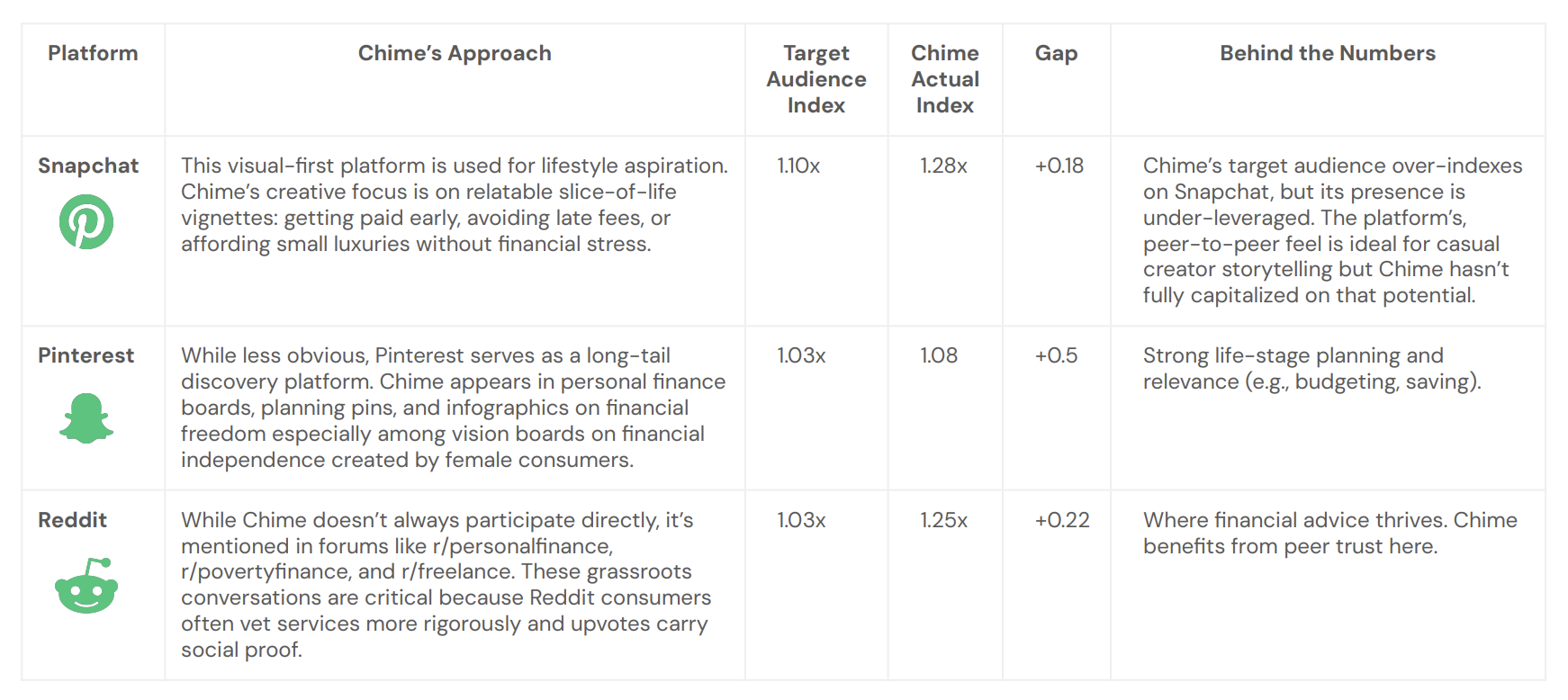

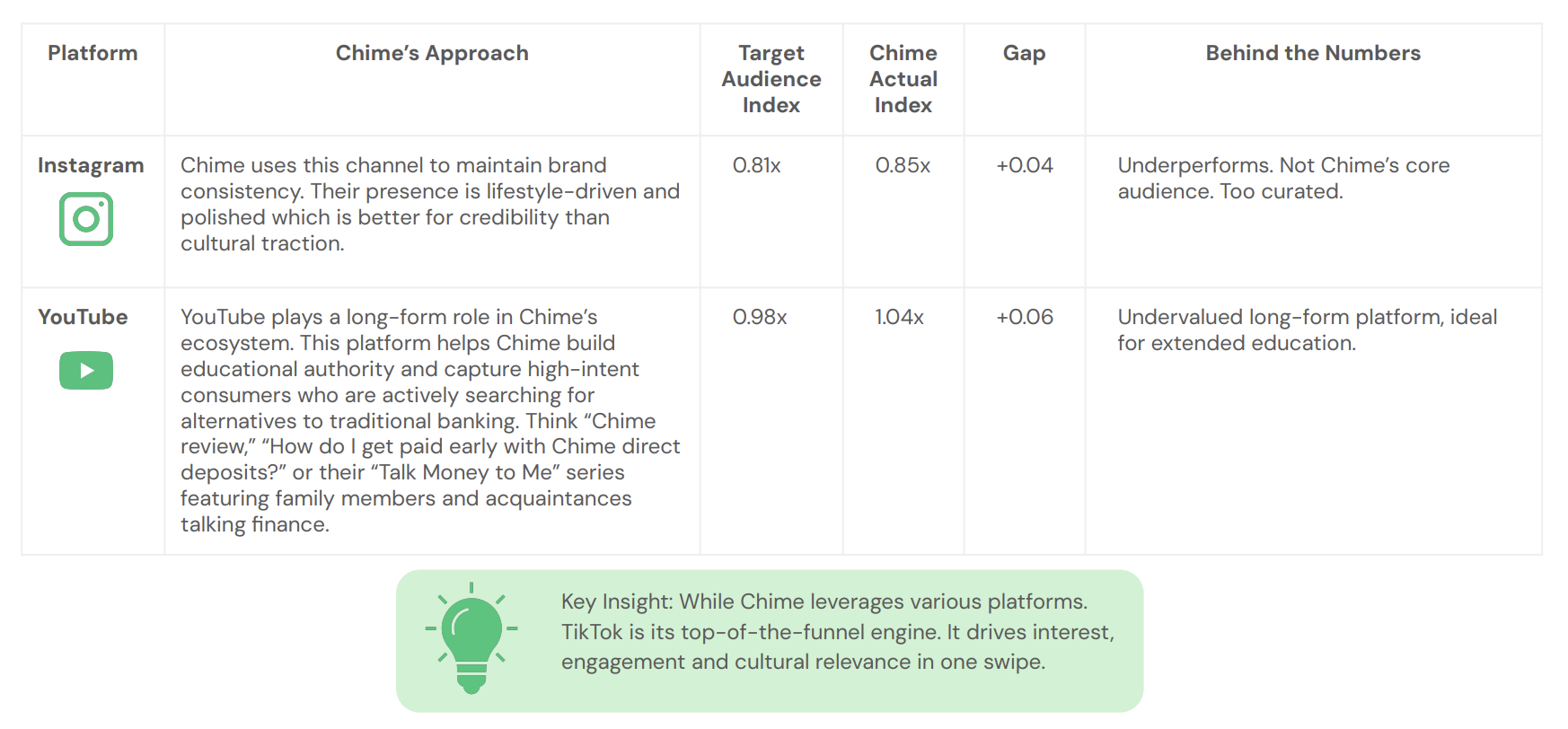

Chime’s Social Platforms Audience Distribution

Chime’s real edge is targeting their core consumers where they scroll. Chime thrives on community-first platforms that deliver viral, digestible financial content whereas many neobanks focus on curated visuals or long-form storytelling.

RightMetric's internal tools analyze digital signals and self-reported data from social media platforms to determine how likely different audience segments are to use each platform. This analysis informs the audience distribution data presented on this slide. Target Audience Index benchmarks Chime's desired audience presence on each platform. Chime Actual Index reveals their actual reach within that audience. A positive gap signifies successful targeting and engagement of core consumers.

Across all platforms, Chime’s ads adopt the language of peer networks: text-message tone, low-polish visuals, and emotional storytelling. On social, it doesn’t speak like a brand. Chime speaks like a friend who figured out a way to game the system and is here to share the hack.

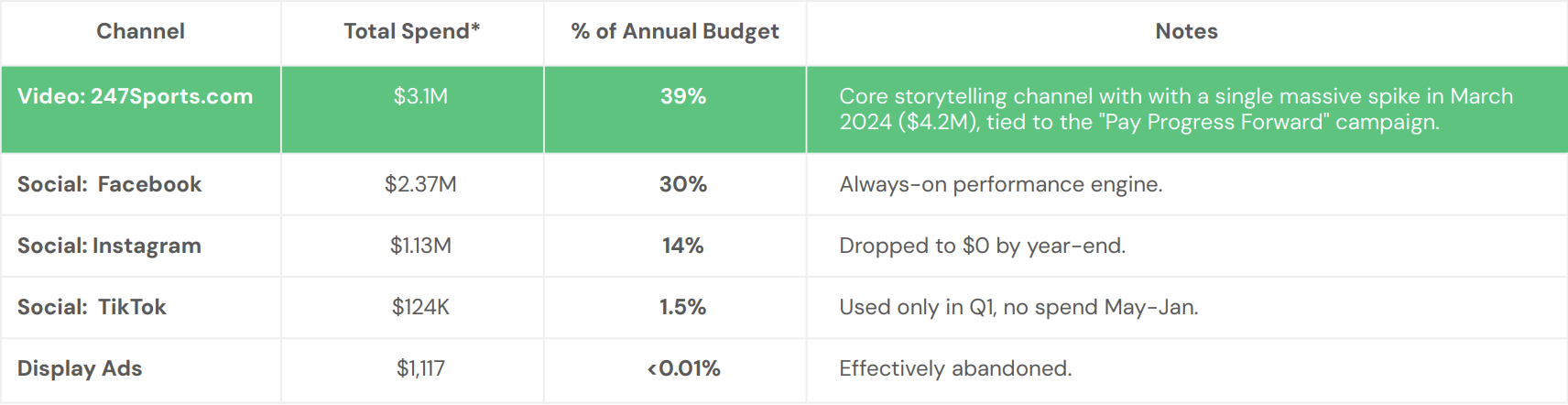

Chime’s Ad Spend By Channel

To better understand how Chime allocates its paid media resources, we broke down the total ad spend by channel and analysed the distribution across the annual budget. This analysis highlights where Chime is investing most heavily — 54% on video ads — revealing key strategic moments (like the spike in video spend tied to a major campaign), and showing shifts in platform focus over the year.

Chime’s ad spend saw a dramatic spike in March 2024, with $5.48M invested—nearly 69% of its total annual budget. This surge was driven by the launch of the Pay Progress Forward campaign, a major brand initiative focused on generosity and financial empowerment.

The campaign centered on a powerful social experiment featuring Wayne Brady and Tiffany "The Budgetnista" Aliche. Participants were given money to pursue a financial goal and asked if they’d share half with someone in need. Every participant chose to give, unlocking a $1M pool to be shared.

Inspired by survey data showing a gap between personal generosity and national perception, the campaign aimed to reframe the narrative and spotlight everyday altruism. It also deepened Chime’s connection with the Black community—one of its strongest and most engaged audience segments.

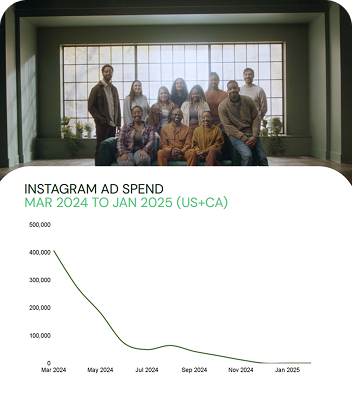

Chime’s spend of $1,117 on display ads across the entire year, suggests a deliberate pivot away from banner/display to native, video, and social channels.

Chime’s Ad Spend By Publisher

Chime's ad spend is laser-focused on dominating niche platforms like 247Sports.com to capture highly engaged, younger demographics. This contrasts sharply with traditional financial institutions' broader channel distribution, signaling Chime's priority for deep engagement and brand resonance within its core audience, rather than casting a wide net.

Chime’s ad spend saw a dramatic spike in March 2024, with $5.48M invested—nearly 69% of its total annual budget. This surge was driven by the launch of the Pay Progress Forward campaign, a major brand initiative focused on generosity and financial empowerment.

The campaign centered on a powerful social experiment featuring Wayne Brady and Tiffany "The Budgetnista" Aliche. Participants were given money to pursue a financial goal and asked if they’d share half with someone in need. Every participant chose to give, unlocking a $1M pool to be shared.

Inspired by survey data showing a gap between personal generosity and national perception, the campaign aimed to reframe the narrative and spotlight everyday altruism. It also deepened Chime’s connection with the Black community—one of its strongest and most engaged audience segments.

Chime’s spend of $1,117 on display ads across the entire year, suggests a deliberate pivot away from banner/display to native, video, and social channels.

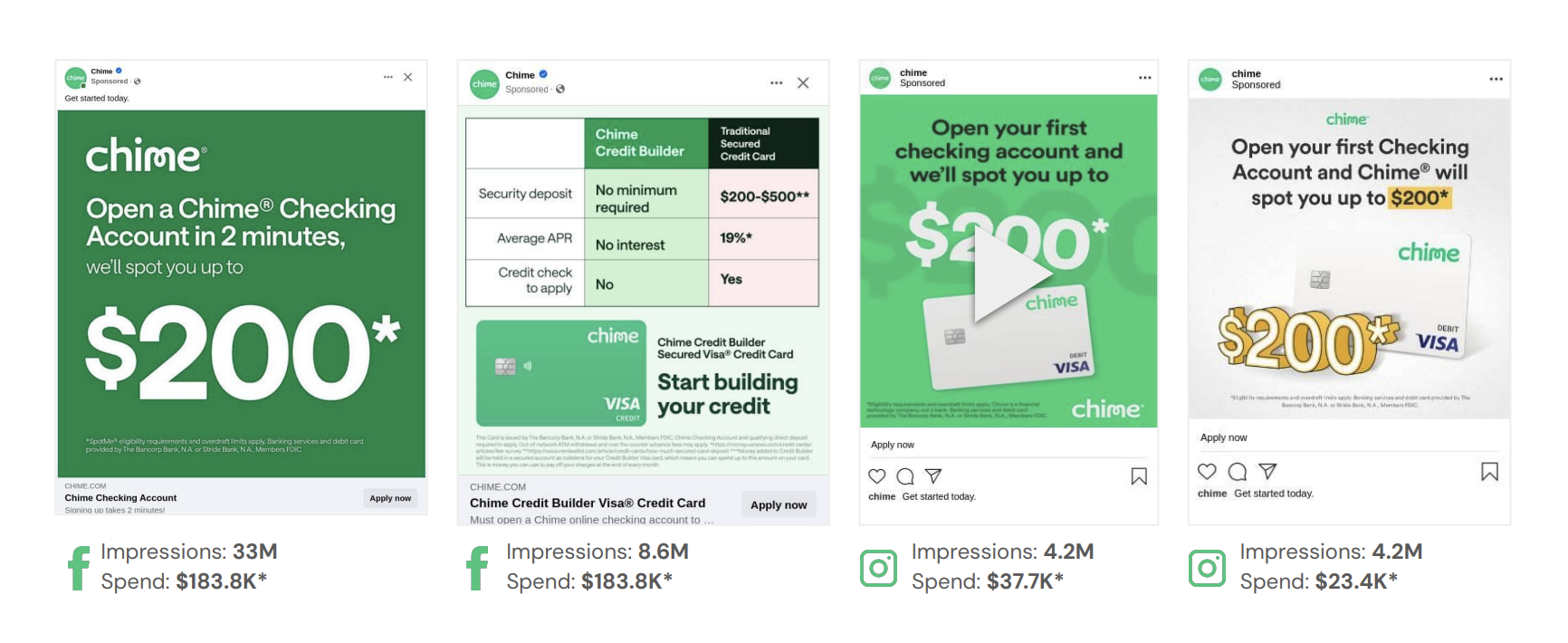

Chime’s Top Performing Ads

On Facebook + Instagram

Chime’s punches above it’s weight

Neobanks like Chime are proving you don’t need a massive budget to make a massive impact. Despite being massively outspent by traditional players like Capital One and US Bank, Chime consistently delivers outsize returns through tight targeting and platform-niche creative. For example, US Bank spent $49M to generate 7.7B impressions.

That’s not a fluke. Through smart placement on video platforms, niche sports publishers and creator-led content, Chime turns modest media budgets into cultural relevance and trust.

Chime’s creatives will likely emphasize real-life relief around:

- Rent timing and payday gaps.

- Budgeting on part-time wages.

- Accessing money instantly in an emergency.

It is also possible that Chime will test Canada-specific features such as CRA-compatible direct deposit tools or early access to government payments. These would mirror its SpotMe and early wage access messaging in the US, adapted for local regulation. If Canadian financial institutions rely solely on polished broadcast-style campaigns, they risk feeling impersonal and out of touch. Chime’s tone of empathy, simplicity, and humor could prove instantly magnetic.

Your cross-platform game plan

Here’s what Canadian financial institutions should takeaway from Chime’s social platform strategy.

Here’s what Canadian financial institutions should takeaway from Chime’s social platform strategy.

What Chime might do in Canada

Chime is likely to replicate its US playbook in the Canadian market, with smart localization. Expect:

What Canadian financial institutions can do next

This chapter delivers a 90-180 day action plan, showing how traditional financial institutions can adapt Chime’s tactics, authentic content, frictionless UX, and empathy-first products, to win back relevance and market share.'

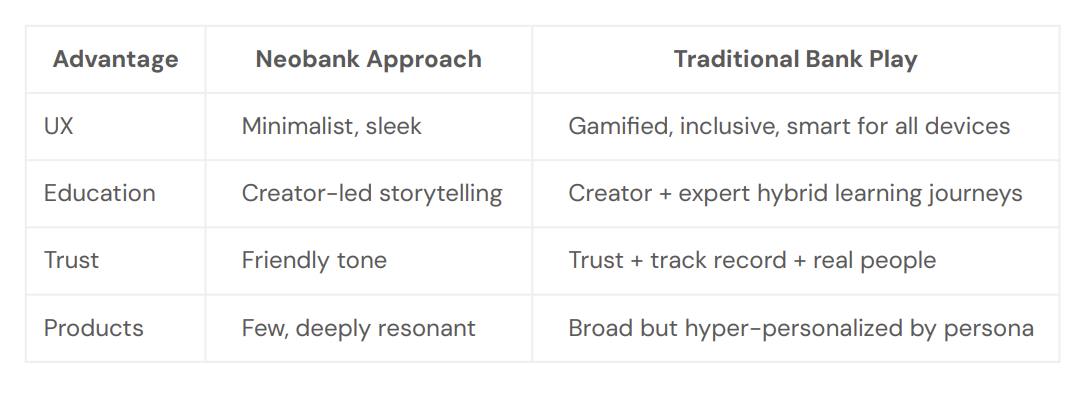

Beat a neobank without becoming one

Chime’s playbook is a wake up call, not a death knell. For Canadian financial institutions, established or emerging, the opportunity isn’t to become Chime, but to learn from it and leverage your own context, precision, and scale to build something even more resonant.

Your Tactical Framework

To thrive in this new banking landscape, Canadian financial institutions must adapt in these four areas.

1. Audience Relevance

Too many financial institutions still build for ideal customers rather than real ones. Neobanks like Chime grow by addressing underserved realities, not aspirations. Canadian institutions need sharper segmentation, localized rollout strategies, and offers tailored to life stages rather than income tiers.

To ensure relevance, traditional financial institutions must lean into security, reliability, and human support.

Key tactics:

- Highlight fraud resolution wins and customer testimonials around safety.

- Offer 24/7 real-time chat with escalation to real agents.

- Launch campaigns around “Your bank for the long run” positioning

2. Platform strategy that reflects attention, not tradition

Chime’s edge comes from platform fluency, not just presence. Canadian financial institutions must stop investing in 'default' channels and start optimizing for where trust is actually built. This means understanding that today's consumers aren't comparing your app to another bank. They're comparing it to Uber, Amazon, and Spotify. Digital fluency is table stakes and friction is fatal.

Key UX enhancements:

- Streamline sign-up flows (e.g., eliminate ID upload friction, preload forms with autofill).

- Introduce gamified savings, “round up” auto-saves.

- Design for low-data consumers and lower-end devices to increase inclusivity

3. Emotional Utility > Product Features

Chime’s success isn’t feature-deep but emotionally sharp. It removes shame, delays, and friction. Traditional financial institutions can build superior products but must frame them through everyday tension and micro relief.

Neobanks’ product designs start with real problems. Traditional financial institutions must do the same. Opportunities for custom offers:

- No-fee “first accounts” for young adults and newcomers.

- Gig economy accounts with early pay, tax tracking, income smoothing.

- Smart student accounts with perks (e.g., Spotify, transit credits, grocery cashback).

SpotMe (free overdraft), Credit Builder and Pay Anyone weren’t just useful, they were differentiated on arrival.

4. Operationalize through UX

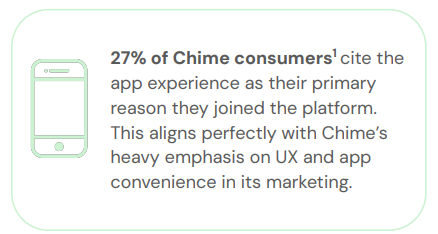

For Chime, 27% of consumers cite the app as their reason for joining. Not marketing. Not product features. The experience itself. Canadian financial institutions don’t need to invent trust. They already have it. But they must express it digitally with empathy, equity, and design built for all devices, all incomes, and all levels of financial fluency.

This is about recalibrating. Chime is a signal, a sign that institutions who translate scale into smart, sensitive, user-first action will define the next era of Canadian finance.

What Canadian FIs should do in the next 90–180 days

For Chime, 27% of consumers cite the app as their reason for joining. Not marketing. Not product features. The experience itself. Canadian financial institutions don’t need to invent trust. They already have it. But they must express it digitally with empathy, equity, and design built for all devices, all incomes, and all levels of financial fluency.

This is about recalibrating. Chime is a signal, a sign that institutions who translate scale into smart, sensitive, user-first action will define the next era of Canadian finance.

Where Neobrands are headed

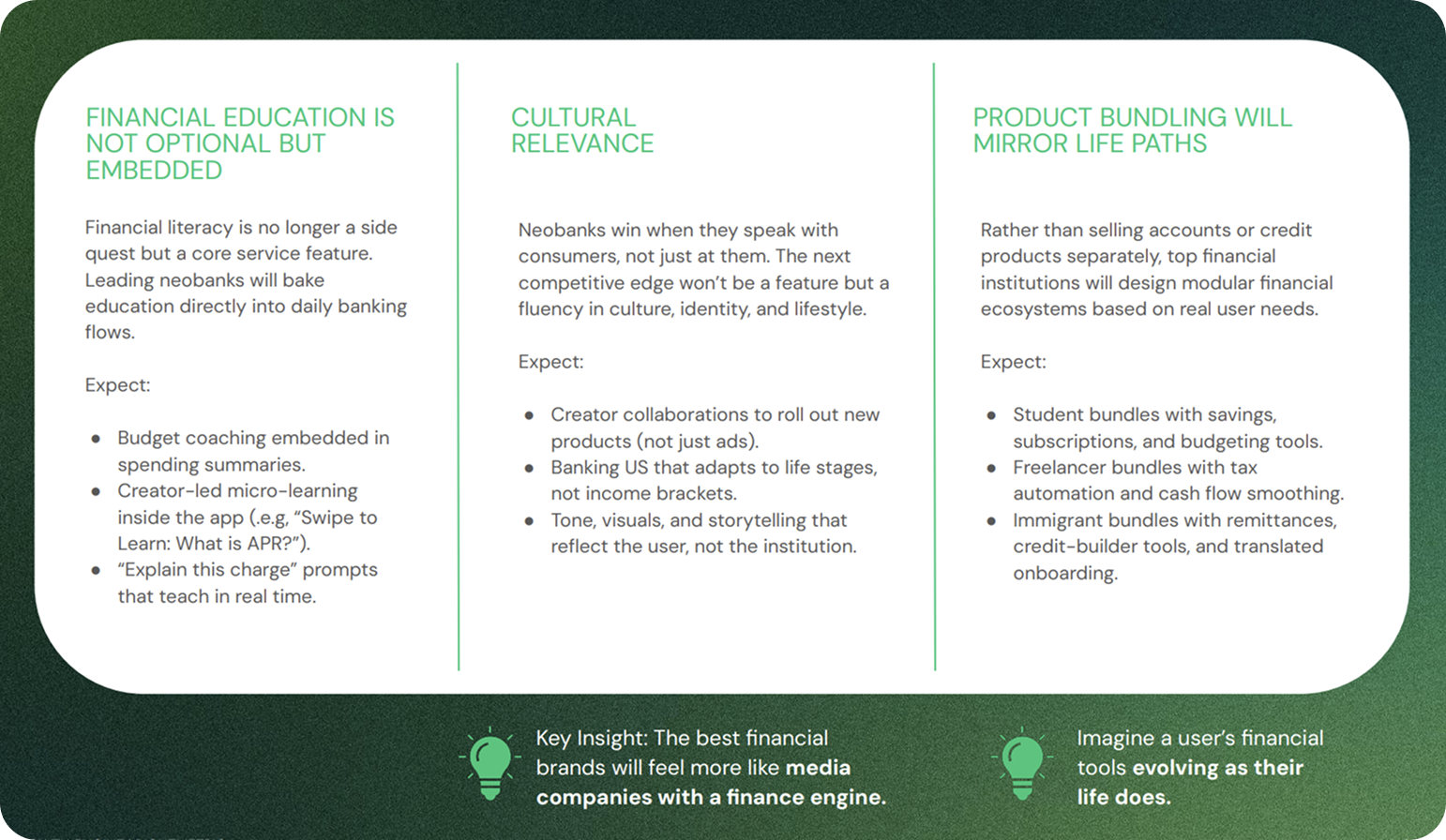

Peek into the future of banking. From AI-powered empathy to embedded education, this chapter explores how neobanks like Chime will continue shaping the next evolution of consumer finance — human, helpful, and hyper-personalized.

Neobanks1 aren’t just changing how we bank, they’re reshaping why we trust. And no one has embodied that shift more than Chime. In just 10 years, Chime has built a model of digital-first, emotionally resonant banking that redefined what financial institutions can be. As we look ahead, Chime, and others following in its footsteps, will continue to evolve, leveraging AI and emerging technologies to deepen personalization, streamline experiences, and expand access.

Human-Digital Hybrids will win the UX arms race

The days of cold automation are numbered. The next-gen neobank isn’t just fast – it’s humanized. We’re entering the era of AI-driven, emotionally intelligent platforms that feel more like financial co-pilots than dashboards.

Expect:

- Personalized financial nudges and “money mood” alerts.

- App journeys guided by creators, not checklists.

- Smart assistants that anticipate and don’t just respond.

UX Evolution Timeline

This is a race to feel most intuitive, not just to most features.

1A closer look at the impact of neobanks on the banking landscape is available in the appendix

The New Rules of Banking

Neobanks didn’t invent better banking, they just listened harder. They built products around pain points, spoke in the language of their consumers, and delivered dignity where bureaucracy once stood.

Whether in Toronto, Lagos, or Berlin, the next generation of banking success will belong to brands that understand three core truths:

- Access is the new loyalty. If consumers can’t get in quickly, clearly, and confidently, they will go elsewhere.

- Empathy is a feature. Design without understanding is noise.

- Culture is currency. Financial institutions that feel native to consumers’ lives will win their wallets and their trust.

What we’re witnessing is a global shift in how people relate to money, institutions, and trust itself.

The winners won’t be the most established or the most digital, they’ll be the most human.

Want to dive deeper?

The insights in this report are just the beginning.

We can help you:

- Refine your target audience strategy: Go beyond basic demographics. Uncover the nuanced preferences and behaviours of key segments like financially stressed individuals and gig workers – the real drivers of Chime's growth.

- Outmaneuver the competition: Analyse playbooks (direct and indirect competitors). Discover your competitors' weaknesses and identify untapped opportunities for differentiation and market share gains.

- Maximize content resonance: Elevate your content from ads to authentic storytelling. Tangible production-level insights to ensure your investments build trust and drive engagement across platforms.

- Optimize your platform strategy for impact: Move beyond "default" channels. Identify and leverage the high-attention platforms where Chime thrives (like TikTok and Reddit) to maximize impact and minimize wasted spend.

Or, tell us your specific questions about competing and winning the next generation of banking customers – we're here to provide insight-driven answers.

RightMetric is your strategic insights partner.

Book a chat with our team.

APPENDIX

Our Data Sources.

We’ve partnered with 25+ of the world’s best marketing data sources, some of which are shown to the right.

Why this matters:

To accurately identify and understand trends, we need holistic data sources that cover all relevant channels on the internet.

Observation isn’t enough to come to robust conclusions. Empirical data must be part of the process. For a deeper dive into our source data—which underpins the findings of this report— check out RightMetric’s “Our Data” page.

APPENDIX

The economic shifts behind Neobank growth

Neobanks are capturing significant online traction, as evidenced by their strong web traffic growth. Traditional banks, on average, are seeing flat performance, indicating a need to revitalize their digital strategies.

Our benchmarking revealed a stark contrast within the traditional banking sector. While most traditional banks either experienced a contraction in web traffic or showed minimal growth (around 2%).

This highlights a clear pathway for traditional institutions: digital innovation can drive substantial growth and engagement, allowing them to effectively compete with neobanks and capture a larger share of the online market.

This graph illustrates the average year-over-year (YoY) traffic growth for neobanks and traditional banks, derived from our keyword search data over a 24-month period (March 2023 - February 2025).

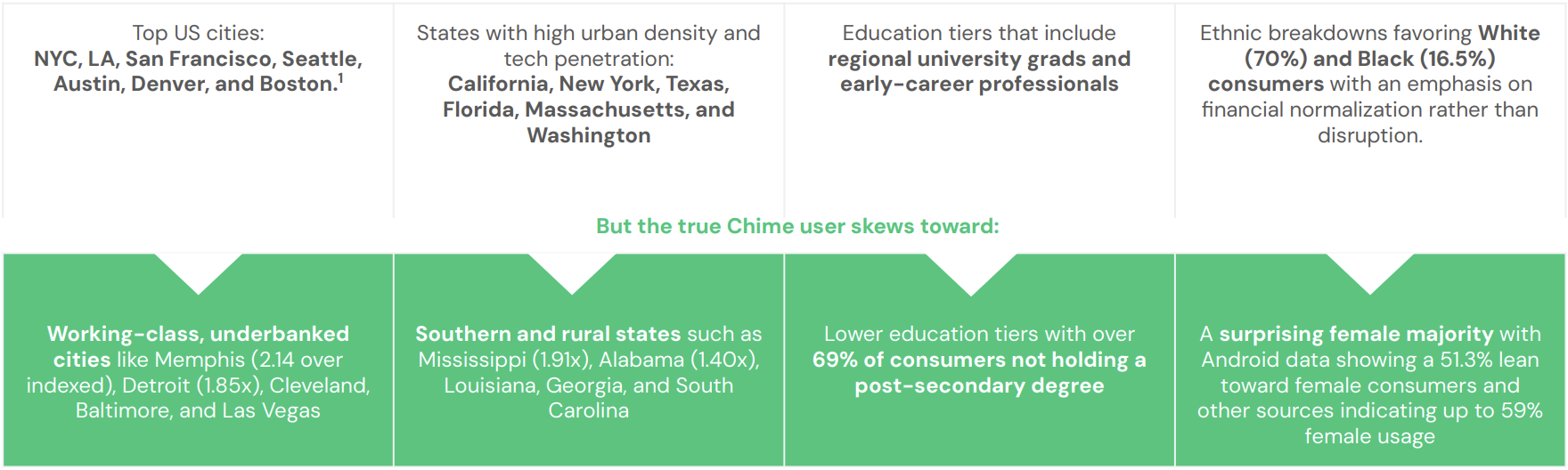

Chime’s product offerings resonate strongly in gig economy hubs like Las Vegas, Atlanta, Dallas, and Memphis, where Chime’s adoption rates significantly exceed the US average.

Chime's popularity in major US cities significantly over-indexes in gig economy hubs like Memphis, TN (2.14x the baseline US population), suggesting they're doing everything right in serving this demographic. Other cities where Chime over-indexed notably include Atlanta, GA (1.41x), Las Vegas, NV (1.41x), and Dallas, TX (1.38x)

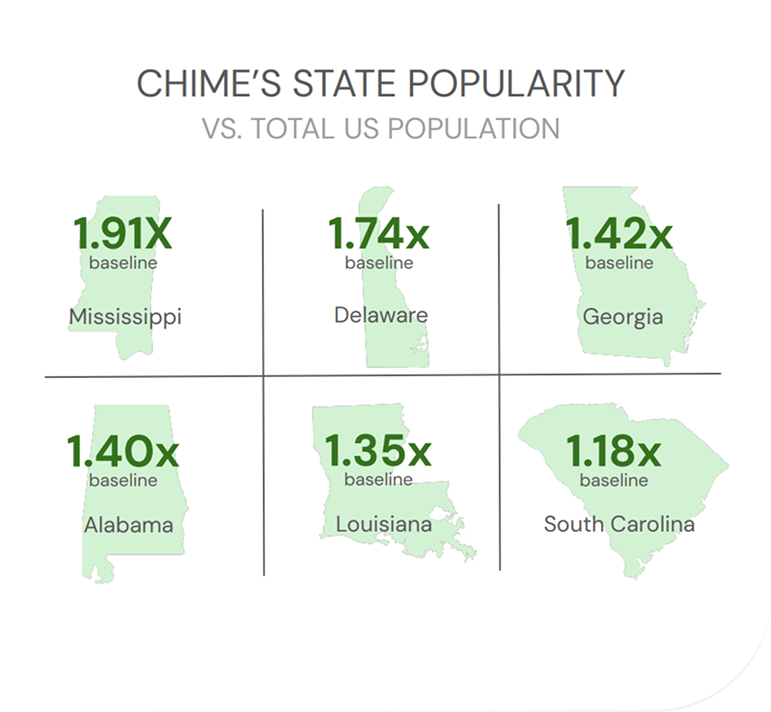

Chime's success extends to working-class and underserved states, where lower-income populations demonstrate a strong preference for low-fee, mobile-first banking solutions.

The significant over-indexing seen in states like Mississippi (1.91x the baseline US population), Delaware (1.74x), and Georgia (1.42x) clearly shows they're doing everything right to meet the needs of these segments.

We also observe considerable over-indexing in Alabama (1.40x), Louisiana (1.35x), and South Carolina (1.18x), further highlighting the effectiveness of their strategy in these regions.

We built a precise US audience profile of Chime's likely customers using social data. This model targets digitally native, financially motivated individuals interested in budgeting, gig work, and challenger banks, revealing their online behaviour and content preferences for targeted strategies.

Complimentary Strategy Session

Take the next step in your market planning. Request your free strategy session today.

Book Your Session →Is the #1 on-demand audience & competitor research service for marketing strategists.

Learn about RESEARCH-ON-DEMAND →